Many Pennsylvanians facing overwhelming debt believe that filing for bankruptcy means handing over their home, car, and savings to creditors. That belief stops countless families from exploring options that could actually protect what they've built. Chapter 13 bankruptcy offers a very different path, one that allows you to keep your property while catching up on missed payments through a structured, court-approved repayment plan. This guide explains exactly how Chapter 13 works in Pennsylvania, what the process looks like from start to finish, and what it genuinely takes to succeed.

Table of Contents

- Understanding Chapter 13 bankruptcy

- How Chapter 13 works: The process explained

- Key factors that affect Chapter 13 success and completion

- Common pitfalls and how to avoid them in Pennsylvania

- A Pennsylvania attorney's perspective: What most guides won't tell you

- Explore your Chapter 13 options with a Pennsylvania attorney

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Chapter 13 defined | Chapter 13 helps you reorganize debt and keep your property through a court-approved repayment plan. |

| Process overview | Expect to follow a 3-5 year repayment plan with regular court oversight in Pennsylvania. |

| Success factors matter | Attorney quality, steady payments, and good faith dramatically affect your success rate. |

| Pitfalls are avoidable | Common mistakes include missed payments and incomplete filings, but proactive legal help can prevent most issues. |

| Local guidance counts | Pennsylvania-specific legal support can improve your chances of successfully completing Chapter 13 bankruptcy. |

Understanding Chapter 13 bankruptcy

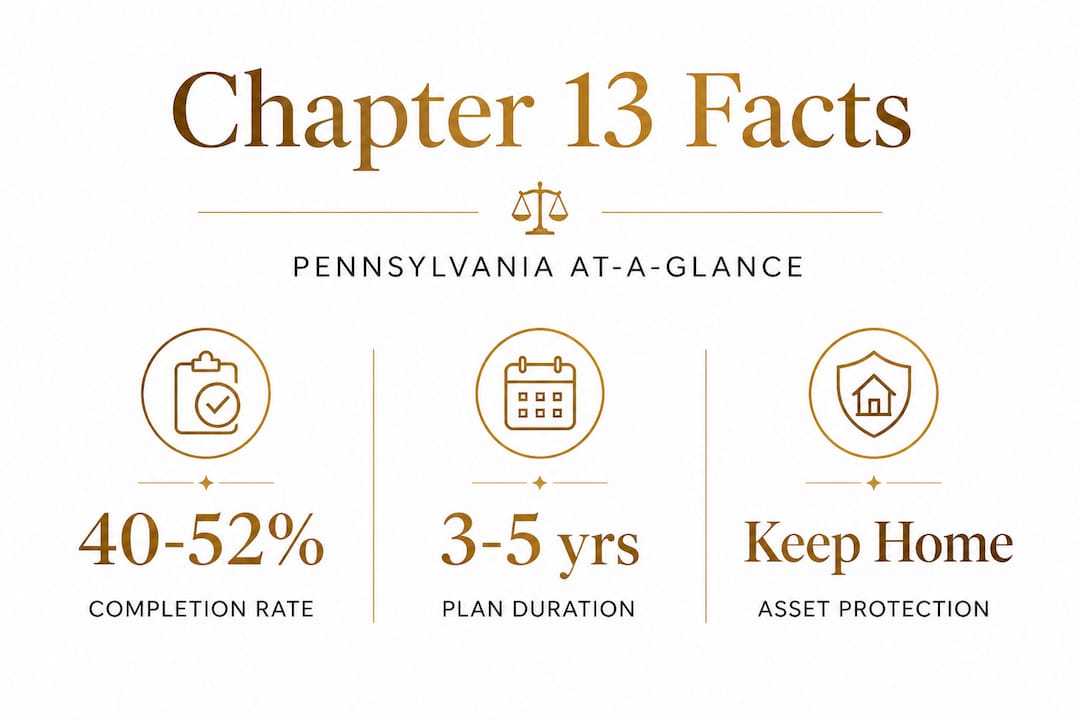

Chapter 13 bankruptcy is often called the "wage earner's plan" because it is designed for individuals with regular income who want to reorganize their debt rather than liquidate their assets. Unlike Chapter 7 bankruptcy, which involves selling non-exempt property to pay creditors quickly, Chapter 13 lets you keep your property while repaying some or all of your debts over a period of three to five years.

To qualify for Chapter 13, you must have a regular source of income and your secured debt (meaning debt backed by collateral, like a mortgage) must be below $1,395,875, while unsecured debt (like credit cards) must fall under $465,275 as of recent federal figures. These limits are periodically adjusted, so confirming current thresholds with an attorney is important. You can review Pennsylvania bankruptcy basics to understand how these eligibility rules apply locally.

Chapter 13 can handle a broad range of debts, though not all of them equally. Here is a breakdown of how different debt types are treated:

- Mortgage arrears: You can catch up on overdue mortgage payments and potentially stop a foreclosure.

- Car loans: Depending on when you financed your vehicle, you may be able to reduce what you owe.

- Priority debts: Taxes owed to the IRS and back child support must generally be paid in full through the plan.

- Unsecured debts: Credit card balances and medical bills may be paid at a reduced percentage, with any remaining balance discharged at the end.

- Student loans: These are rarely dischargeable and typically survive the plan intact.

One notable detail for Pennsylvania filers is that the state's exemption laws, which protect certain assets from creditors, interact with Chapter 13 plans in ways that affect how much you must pay unsecured creditors. Specifically, you must pay unsecured creditors at least as much as they would have received if you had filed Chapter 7 instead. This is called the "best interest of creditors" test, and getting this calculation right requires careful legal analysis. Residents in central Pennsylvania can also look into Bellwood-area bankruptcy solutions for local guidance specific to their region.

Nationally, completion rates for Chapter 13 hover between 40% and 52%, meaning that between 48% and 60% of cases are dismissed before the filer receives a discharge. These numbers underscore that Chapter 13 is not a simple process, and the quality of legal representation is consistently identified as a key factor in whether filers succeed.

Pro Tip: If your primary goal is saving your home from foreclosure, Chapter 13 is often far superior to Chapter 7. It gives you the legal mechanism to catch up on arrears while staying in the house, something Chapter 7 cannot do.

| Debt type | Treatment in Chapter 13 |

|---|---|

| Mortgage arrears | Can be repaid over plan duration |

| Car loan (recent) | May need full repayment |

| Credit card debt | Partial repayment possible |

| IRS tax debt (recent) | Must be repaid in full |

| Student loans | Rarely dischargeable |

| Child support arrears | Must be repaid in full |

How Chapter 13 works: The process explained

Knowing what Chapter 13 is matters, but understanding what it actually feels like to go through it in Pennsylvania prepares you to make a confident decision. The process involves several distinct stages, each with its own requirements and deadlines.

-

Initial consultation and eligibility review. Your attorney evaluates your income, debts, and assets to determine whether Chapter 13 is appropriate and how your plan should be structured.

-

Filing the petition. You file your bankruptcy petition with the appropriate federal bankruptcy court. Pennsylvania has three districts: Eastern, Middle, and Western. Once you file, an automatic stay immediately takes effect. This legal protection halts most collection actions, including foreclosures, repossessions, lawsuits, and wage garnishments.

-

Proposed repayment plan submission. You submit your Chapter 13 repayment plan, which must be filed within 14 days of the petition. The plan outlines how much you will pay each month, which creditors are being paid, and in what order.

-

Meeting of creditors (341 meeting). Roughly three to six weeks after filing, you attend a brief meeting where the bankruptcy trustee and any creditors who choose to appear can ask questions about your finances under oath. Most meetings last only a few minutes with proper preparation.

-

Confirmation hearing. A bankruptcy judge reviews your plan to confirm it meets all legal requirements. Creditors can object. Importantly, courts can reject plans for lack of good faith even if the plan appears technically compliant on paper. This is a subtle but critical legal standard.

-

Making plan payments. Once confirmed, you begin making monthly payments to the trustee, who distributes funds to creditors. Plans run between 36 and 60 months depending on your income relative to the Pennsylvania median.

-

Discharge. After completing all required payments and satisfying other conditions (like completing a financial management course), the court issues a discharge, eliminating any remaining dischargeable debt.

Understanding the role of a bankruptcy attorney throughout this process is essential. Errors in the plan, incomplete disclosures, or failure to respond to trustee objections can derail the entire case before it ever reaches confirmation.

Pro Tip: Payments often begin within 30 days of filing, even before the plan is formally confirmed. Setting up automatic bank transfers from the start reduces the risk of accidental missed payments during those early critical months.

Key factors that affect Chapter 13 success and completion

Understanding the path is only half the story. Knowing the realistic odds helps Pennsylvanians make decisions based on facts rather than assumptions.

The most important national data point is the completion rate by district, which reveals dramatic variation across the country. Some districts in Massachusetts report completion rates as high as 97%, while certain Tennessee districts fall to around 54%. Pennsylvania's rates generally fall within the national mid-range, but district-specific patterns still exist between the Eastern, Middle, and Western districts.

"Attorney quality is consistently identified as the single most important variable in whether a Chapter 13 case reaches discharge. Filers without legal representation face significantly higher dismissal rates across all districts."

Several factors drive those differences. They include:

- Attorney quality and experience. An attorney who knows the local trustee's expectations and the judge's tendencies can draft a plan that clears confirmation more smoothly.

- Accurate income disclosure. Trustees scrutinize income figures carefully. Overstating or understating income creates grounds for objection or dismissal.

- Consistent payments. Missing even one payment can give the trustee grounds to seek dismissal. Courts can allow modifications for genuine hardship, but this is not automatic.

- Good faith in plan structure. Courts evaluate whether the plan reflects an honest effort to repay creditors, not just a strategy to shield assets from obligation.

- Change in financial circumstances. Job loss, divorce, or medical emergencies during the plan period are among the most common reasons plans fail. Knowing you can request a modification before missing a payment is critical.

| District/Region | Approximate completion rate |

|---|---|

| Massachusetts (high) | ~97% |

| Pennsylvania (estimate) | ~45-55% |

| Tennessee (low) | ~54% |

| National average | ~40-52% |

Note: Figures are approximations based on available district data and may shift year to year.

The path to rebuilding after bankruptcy begins with completing the plan, which makes maximizing the chance of success a financial priority, not just a legal one. Every dismissed case means lost filing fees, continued creditor pressure, and a damaged credit record without the benefit of a discharge.

Common pitfalls and how to avoid them in Pennsylvania

With realistic expectations now established, it is worth addressing what actually causes Chapter 13 plans to fail and how you can prevent those outcomes in your case.

The most common reasons plans are dismissed or fail to reach discharge include:

- Missed or late payments. This is the leading cause of dismissal. Courts and trustees have limited patience for payment lapses, and plans are dismissible for missed payments without exception.

- Failure to disclose all income and assets. Bankruptcy courts require complete financial transparency. Omitting a side income stream or an asset you forgot to list can lead to plan denial or, worse, allegations of fraud.

- Not filing required tax returns. Chapter 13 filers must be current on all federal and state tax returns. Unfiled returns can block confirmation and lead to dismissal.

- Creditor objections going unanswered. If a creditor objects to your plan and your attorney fails to respond timely, the court may deny confirmation.

- Plans rejected for lack of good faith. Even technically compliant plans can be denied if the court concludes the filer is not making a genuine effort to repay creditors. This is a judgment call with real consequences.

Concrete steps to stay on track include:

- Set up automatic payments to your trustee from day one. Do not rely on manual transfers.

- Notify your attorney immediately if your income drops or expenses spike unexpectedly. A hardship modification may be available before a missed payment occurs.

- File all required state and federal tax returns promptly each year during the plan.

- Keep detailed records of every payment made and every communication with your trustee.

- Review your bankruptcy recovery plan with your attorney at least annually to identify any needed adjustments.

Pro Tip: If your financial situation changes significantly (job loss, a medical emergency, or a major unexpected expense), contact your attorney before you miss a payment. Proactive modification requests are far more likely to succeed than reactive ones filed after the trustee has already moved to dismiss your case.

A Pennsylvania attorney's perspective: What most guides won't tell you

Most Chapter 13 guides focus on procedures and eligibility. What they rarely address is the informal reality that significantly shapes outcomes for Pennsylvania filers.

Here is an honest perspective: Chapter 13 is a five-year commitment to living within a tightly constrained budget while a trustee monitors your finances. Many people underestimate just how demanding that is, not legally, but practically. Life changes. Unexpected expenses arrive. What feels manageable at filing can become genuinely burdensome by year three.

The filers who succeed are not necessarily those with the smallest debt loads or the most stable income at the time of filing. They are the ones who treat the plan as an active, ongoing obligation rather than a set-it-and-forget-it process. They stay in regular contact with their attorney, flag problems early, and take the modification process seriously when circumstances change.

There is also a persistent myth that court confirmation is a formality once you submit a compliant plan. It is not. The "good faith" standard gives judges real discretion to reject plans that appear designed to minimize creditor recovery without justification. Courts look at the totality of your financial behavior, including how you incurred the debt, what efforts you made before filing, and how the plan balances your needs against what you genuinely can repay. This is where the quality of your legal representation matters most. An experienced attorney does not just fill out forms. They anticipate trustee objections, respond to creditor concerns, and frame your plan in a way that reflects honest intent.

Another underappreciated reality: not every Pennsylvania bankruptcy district is the same. Trustees in different districts have different priorities and tendencies. An attorney who practices regularly in your district knows those tendencies and uses them strategically when structuring your plan.

Explore your Chapter 13 options with a Pennsylvania attorney

Taking the first step toward financial relief is often the hardest part, especially when the rules feel complex and the stakes feel high. The good news is that you do not have to navigate Pennsylvania's Chapter 13 process alone.

Working with a local Pennsylvania bankruptcy attorney means getting guidance tailored to your actual district, your specific debts, and your personal financial situation. Understanding local trustee expectations and court practices gives you a meaningful advantage in getting your plan confirmed and completed. If you are ready to explore your options, reviewing the Pennsylvania bankruptcy solutions available through this practice is a strong first step. For those in central Pennsylvania, dedicated Bellwood bankruptcy help is also available for a more locally focused consultation. Do not let uncertainty hold you back from a path that could protect your home and reset your financial future.

Frequently asked questions

What debts are not discharged in Chapter 13 bankruptcy?

Certain debts like child support, alimony, and most student loans are not discharged under Chapter 13. Recent income tax debt and debts arising from fraud are also generally excluded from discharge.

How long does a Chapter 13 bankruptcy last in Pennsylvania?

A typical Chapter 13 plan lasts 3 to 5 years, depending on your income and repayment structure. Filers with income above the Pennsylvania median are generally required to commit to the full 60-month plan.

What happens if I miss a Chapter 13 payment?

Your plan could be dismissed for missed payments, but courts sometimes allow modifications if you act quickly and demonstrate genuine hardship. Contacting your attorney immediately is the most important step you can take.

Can my Chapter 13 plan be rejected even if I follow all the rules?

Yes, a plan can be rejected for lack of good faith even if it is otherwise technically compliant with all legal requirements. Courts evaluate whether the overall structure of the plan reflects an honest effort to repay creditors.

What factors improve the odds of successfully completing Chapter 13?

The quality of your attorney, making consistent payments, and filing in the right district all meaningfully impact your completion rate. Proactive communication with your attorney and trustee throughout the plan also plays a significant role in long-term success.