When financial pressure builds to the breaking point, many Pennsylvania residents believe bankruptcy means handing over their home, their car, and everything they've worked for. That belief stops people from exploring a legal tool that could genuinely change their situation. Chapter 7 bankruptcy is not a punishment. It is a federally protected process that can eliminate large amounts of unsecured debt, stop creditor calls immediately, and give qualifying individuals a real financial reset. This guide explains what Chapter 7 is, who qualifies under Pennsylvania rules, how it compares to other debt relief options, and what happens after the process ends.

Table of Contents

- Chapter 7 bankruptcy: What it is and how it works

- Who qualifies for Chapter 7 bankruptcy in Pennsylvania?

- Chapter 7 vs. other Pennsylvania debt relief options

- Life after Chapter 7 bankruptcy: What to expect

- What most people miss about Chapter 7 bankruptcy in Pennsylvania

- Take the next step toward financial freedom

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Chapter 7 protects basics | Most people filing Chapter 7 keep essential property like their home and car. |

| Eligibility follows income rules | You must meet Pennsylvania’s income test or have low disposable income to qualify. |

| Not all debts are erased | Some debts like taxes, child support, or student loans cannot be discharged. |

| Life after bankruptcy is possible | You can rebuild credit and financial stability after completing Chapter 7. |

| Comparing options is key | Understand all debt relief choices before choosing Chapter 7 bankruptcy. |

Chapter 7 bankruptcy: What it is and how it works

Chapter 7 bankruptcy is a legal process governed by federal law that allows individuals to discharge, or permanently eliminate, most types of unsecured debt. Unsecured debt is money owed without collateral backing it, including credit card balances, medical bills, utility arrears, and personal loans. Once a discharge is granted, creditors can no longer legally pursue collection on those debts.

The process typically takes three to six months from the date of filing to final discharge. That speed is one reason Chapter 7 is often called "liquidation bankruptcy." A court-appointed trustee reviews the filer's assets, and any property that falls outside legal exemption limits can technically be sold to partially pay creditors. In practice, most filers in Pennsylvania have little to no non-exempt property, meaning the trustee finds nothing to liquidate and the case closes with debts wiped clean.

Understanding protecting your assets during bankruptcy is one of the first things a filer should research, because Pennsylvania offers both federal and state exemptions that can shield a home's equity, a vehicle, retirement accounts, household goods, and tools of your trade.

Debts that Chapter 7 can eliminate:

- Credit card balances

- Medical and hospital bills

- Personal loans and payday loans

- Utility and lease arrears

- Certain older tax debts (subject to specific conditions)

Debts that Chapter 7 cannot eliminate:

- Most federal and state student loans

- Recent income taxes (generally taxes owed within the past three years)

- Child support and alimony obligations

- Debts arising from fraud or intentional wrongdoing

- Criminal fines and restitution orders

Means test snapshot: Eligibility requires passing the means test: income below the Pennsylvania median, which in 2026 is approximately $55,404 for a single-person household and $97,140 for a family of four, or low disposable income after allowed deductions.

Steps in the Chapter 7 process:

- File a petition and financial schedules with the bankruptcy court

- Trustee reviews your assets, income, and debts

- Attend the meeting of creditors (a brief, relatively informal hearing)

- Complete a debtor education course

- Receive the discharge order, typically within 60 to 90 days after the creditors meeting

The automatic stay is one of the most immediate benefits. The moment you file, all collection actions including lawsuits, wage garnishments, and creditor phone calls must stop by law.

Who qualifies for Chapter 7 bankruptcy in Pennsylvania?

Eligibility for Chapter 7 is not automatic. Congress created the means test in 2005 to ensure the process is used by people who genuinely cannot repay their debts, not by those who could manage a structured repayment plan. Passing the means test for Chapter 7 is the single most important eligibility hurdle.

How the means test works, step by step:

- Calculate your average monthly income over the six months before filing and multiply by 12 to get your annual figure

- Compare that figure to Pennsylvania's median income for your household size

- If you're below the median, you automatically qualify and no further testing is needed

- If you're above the median, deduct allowable expenses (IRS standards for food, housing, healthcare, and certain secured debt payments) to calculate your monthly disposable income

- Assess whether your disposable income is low enough to pass the second part of the test

Pennsylvania median income figures for 2026:

| Household size | Annual median income |

|---|---|

| 1 person | $55,404 |

| 2 people | $74,220 |

| 3 people | $86,900 |

| 4 people | $97,140 |

| Each additional person | Add approximately $9,900 |

Consider two scenarios. A single individual in Altoona earning $48,000 per year in gross wages falls below the $55,404 threshold and automatically passes. A family of five earning $108,000 per year falls above the median for their household size, but after deducting mortgage payments, health insurance premiums, vehicle loan payments, and childcare costs, their disposable income may fall low enough to still qualify.

Pro Tip: Keep at least six months of pay stubs, bank statements, and receipts for all major expenses before you file. Detailed, organized records give your attorney the best picture of your financial situation and make it easier to document every allowable deduction, which can be the difference between qualifying and not qualifying.

If you do not qualify for Chapter 7, you are not out of options. Many Pennsylvania residents who fail the means test can still pursue Chapter 13 bankruptcy alternative, which involves a structured three to five year repayment plan rather than immediate discharge.

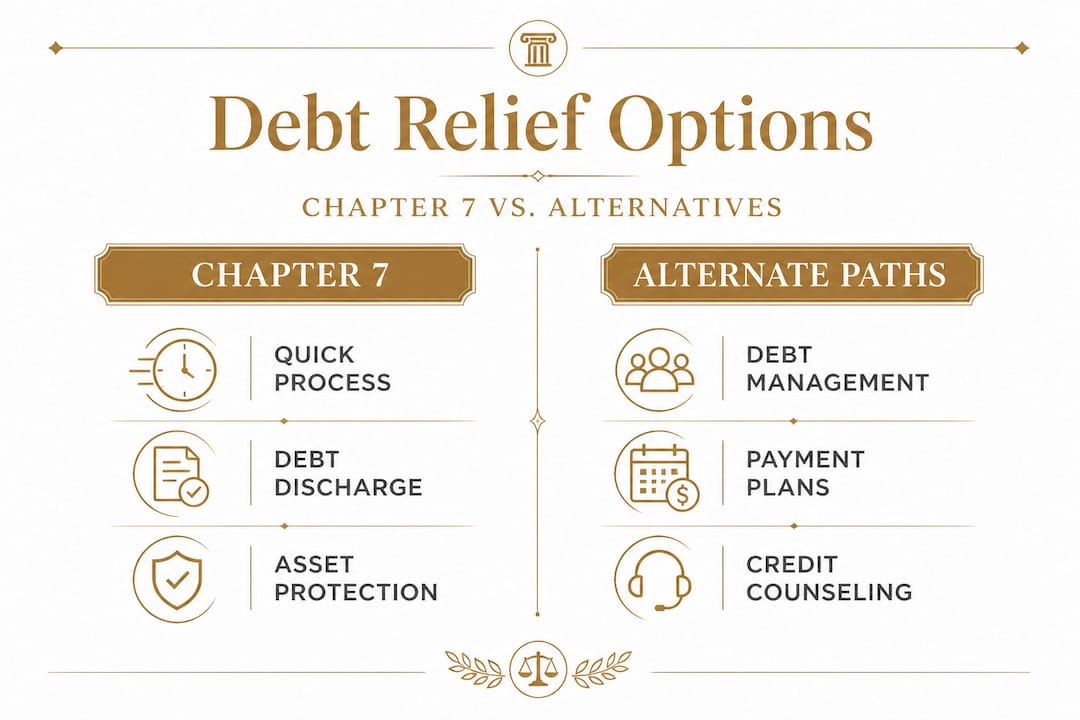

Chapter 7 vs. other Pennsylvania debt relief options

Choosing the right debt relief strategy depends on your income, assets, the types of debt you carry, and your long-term financial goals. Chapter 7 is powerful, but it is not the right fit for everyone. Here is how it stacks up against the two most common alternatives.

Comparison of debt relief options:

| Feature | Chapter 7 | Chapter 13 | Debt management plan |

|---|---|---|---|

| Eligibility | Must pass means test | No income cap | No legal requirement |

| Timeline | 3 to 6 months | 3 to 5 years | 3 to 5 years |

| Asset risk | Non-exempt assets may be sold | Keep all assets if plan is followed | No asset risk |

| Debt discharged | Most unsecured debt eliminated | Partial or full repayment required | Negotiated reduction |

| Effect on credit | Stays on report 10 years | Stays on report 7 years | Less severe impact |

| Stops collections | Yes, immediately | Yes, immediately | Only if creditors agree |

| Best for | Low income, limited assets | Regular income, assets to protect | Mild to moderate debt |

Chapter 7 may be the better fit if you:

- Have primarily unsecured debts you cannot realistically repay

- Have little non-exempt property to protect

- Need fast resolution and cannot sustain a multi-year repayment plan

- Are below or close to Pennsylvania's median income threshold

Chapter 7 may not be the right fit if you:

- Are behind on a mortgage and want to stop foreclosure while catching up

- Earn above the median and cannot pass the full means test

- Carry significant non-exempt assets you would lose in liquidation

- Recently received a large inheritance or financial windfall

One common misconception is that a debt management plan (DMP) run through a nonprofit credit counseling agency is always the gentler alternative. A DMP does not discharge debt. It restructures payment terms with creditor agreement, meaning if even one major creditor refuses to participate, the plan may not address your full situation. The Chapter 13 debt repayment option provides a court-ordered structure that binds all creditors, which is a meaningful difference when dealing with aggressive lenders.

Another misunderstanding involves which debts each option covers. Neither bankruptcy chapter eliminates student loans under normal circumstances. Many people assume filing automatically clears all debts and are blindsided when certain obligations survive discharge. Knowing which debts will remain gives you a clearer picture of what your finances will look like post-filing, which is critical for realistic planning.

Life after Chapter 7 bankruptcy: What to expect

Receiving a discharge order is a significant moment. It means the legal obligation on most of your listed debts is permanently removed. But that moment is a starting line, not a finish line. How you manage your finances in the months and years following discharge will determine how quickly you recover and how strong your financial future becomes.

Chapter 7 stays on your credit report for up to 10 years from the filing date. That sounds discouraging, but it does not mean credit is unavailable for a decade. Many filers begin qualifying for secured credit cards within a few months of discharge, and some obtain car loans within one to two years. Lenders know that a person who has discharged their debts actually has less outstanding liability than someone drowning in unpaid balances.

Steps to rebuild after Chapter 7 discharge:

- Review your credit reports from all three bureaus to confirm discharged debts are correctly reported as zero balance

- Create a realistic monthly budget that accounts for all current income and necessary expenses

- Open a secured credit card and use it for small, routine purchases you pay off every month

- Build a small emergency fund of at least $500 to $1,000 to prevent future debt spiral from unexpected expenses

- Monitor your credit score monthly using free tools and dispute any errors immediately

- Consult a financial counselor if you are unsure how to structure savings, especially around retirement contributions

Pro Tip: Do not apply for multiple credit accounts simultaneously after discharge. Each hard inquiry lowers your score slightly, and the pattern of rapid new account openings can signal risk to lenders. One well-chosen secured card, managed responsibly, builds credit far more effectively.

It is worth revisiting the limitations of Chapter 7 as you plan your next steps. Obligations like child support, recent income taxes, and student loans survive discharge. If those debts are significant, address them directly with a payment plan or a negotiated settlement rather than assuming they will fade on their own. Understanding rebuilding after bankruptcy and having a concrete plan for those surviving debts is just as important as the discharge itself.

What most people miss about Chapter 7 bankruptcy in Pennsylvania

After working through bankruptcy matters in Pennsylvania, one pattern stands out clearly. The fear of losing everything keeps people trapped in debt for years longer than necessary. In reality, the vast majority of Chapter 7 filers keep their home, their car, their retirement savings, and their household belongings. Pennsylvania's exemption laws, combined with federal exemptions, protect far more than most people realize.

The real risk after Chapter 7 is not starting over with nothing. The real risk is getting the discharge and then returning to the same financial habits that led to the crisis. The discharge gives you a clean slate; what you write on it next determines everything.

The subtler pitfalls are where people actually stumble. Transferring assets to a family member in the months before filing to "protect" them can be reversed by the trustee as a fraudulent transfer and could jeopardize the entire case. Failing to list a debt because you assume it will be forgiven anyway can cause that specific debt to survive discharge. And ignoring non-bankruptcy options entirely, like negotiating directly with a hospital for a reduced medical bill or setting up an IRS installment agreement, means some people file when they did not need to.

Another underappreciated point is that valuable attorney guidance is not just about paperwork. An experienced bankruptcy attorney in Pennsylvania will spot issues you would never find on your own, from calculating the correct exemption amounts to identifying which debts require special handling. A filing error can delay discharge, trigger trustee scrutiny, or in serious cases result in denial of discharge altogether. The stakes are real, and the nuances matter.

Take the next step toward financial freedom

If you are weighing your options and wondering whether Chapter 7 is the right path, the most important next step is a conversation with someone who knows Pennsylvania bankruptcy law inside and out.

Every bankruptcy case is different. Your income, your assets, the types of debt you carry, and your long-term goals all shape which strategy will deliver the best outcome. At pennsylvaniadui.attorney, you can get personalized guidance from an experienced attorney who handles bankruptcy cases across Pennsylvania. Whether you need a full eligibility review or simply want to understand your options, Pennsylvania bankruptcy law help is available for residents throughout the state. If you are located in central Pennsylvania, dedicated Bellwood bankruptcy services and Brownsville bankruptcy help connect you with local, knowledgeable support. Do not let confusion about the process keep you in financial pain longer than necessary.

Frequently asked questions

Will I lose my home or car if I file Chapter 7 bankruptcy in Pennsylvania?

Most filers keep their primary home and vehicle, as long as the equity in those assets falls within exemption limits and they remain current on secured payments. Pennsylvania allows filers to choose between state and federal exemption sets, which can provide significant protection for essential property.

What debts does Chapter 7 bankruptcy eliminate?

Chapter 7 typically wipes out credit card balances, medical bills, and personal loans, but does not eliminate student loans, recent income taxes, or child support obligations. Understanding which debts will survive before you file helps you set accurate expectations for your post-discharge financial situation.

How long does a Chapter 7 bankruptcy affect my credit?

A Chapter 7 filing appears on your credit report for up to 10 years from the filing date, but many filers begin rebuilding their credit score meaningfully within one to two years of discharge by using secured credit products responsibly.

Can I file for Chapter 7 bankruptcy more than once?

You must wait at least eight years from your previous Chapter 7 discharge before filing for Chapter 7 again, though other debt relief options may be available sooner depending on your circumstances.

What if I don't qualify for Chapter 7 bankruptcy?

If you do not pass the means test requirements, you may still be eligible for Chapter 13 bankruptcy, which allows you to repay debts over three to five years under a court-approved plan while keeping your assets protected.