Bankruptcy is not a one-size-fits-all solution, and for Pennsylvanians struggling with overwhelming debt, assuming it is can lead to a costly mistake. Whether you are facing foreclosure, drowning in credit card balances, or dealing with medical bills that never seem to shrink, the chapter you file under will shape your financial future in fundamentally different ways. Chapter 7 and Chapter 13 each follow distinct rules, timelines, and outcomes, and picking the wrong path can mean losing property you could have saved or spending years in a repayment plan when a faster discharge was possible. This guide breaks down both options clearly so you can walk into that first consultation already informed.

Table of Contents

- Understanding bankruptcy basics in Pennsylvania

- Key differences: Process, timeline, and property impact

- Who qualifies for Chapter 7 or Chapter 13 in Pennsylvania?

- Property and payments: How exemptions shape your path

- Success rates, risks, and real-life outcomes

- Beyond the basics: What most guides miss about Chapter 7 vs. 13 in Pennsylvania

- Get guidance for your Pennsylvania bankruptcy decision

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

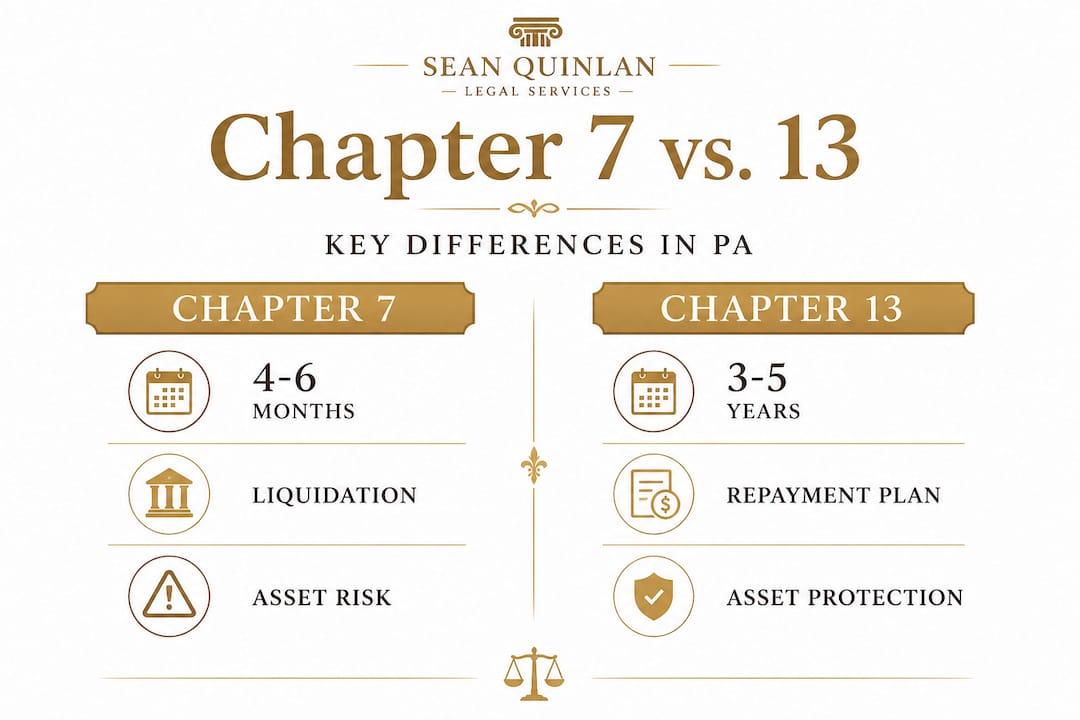

| Chapter 7 is quickest | Most Pennsylvanians finish Chapter 7 in four to six months with qualifying debts wiped out. |

| Chapter 13 protects assets | A three- to five-year plan can help you keep your home and other valuables if you're behind on payments. |

| Eligibility depends on income | The means test or regular income determines which chapter you can use and your best odds for relief. |

| Exemptions influence outcomes | Pennsylvania's property exemptions can impact what you keep versus lose in bankruptcy. |

| Completion rates vary | Chapter 13 success rates are lower, with fewer than half of cases reaching discharge, so planning is critical. |

Understanding bankruptcy basics in Pennsylvania

Bankruptcy is a federal legal process that gives individuals a structured way to address debts they cannot reasonably repay. Two chapters of the U.S. Bankruptcy Code apply most directly to individuals in Pennsylvania: Chapter 7 and Chapter 13.

Chapter 7 is often called "liquidation bankruptcy." It works by having a court-appointed trustee review your assets, potentially sell non-exempt property, and use the proceeds to pay creditors. In exchange, most remaining qualifying debts are discharged, meaning you are no longer legally obligated to pay them. As legal guidance explains, Chapter 7 discharges qualifying debts without a repayment plan, typically wrapping up within a few months.

Chapter 13, by contrast, is a reorganization approach. Rather than wiping the slate clean quickly, you propose a structured repayment plan supervised by the bankruptcy court. According to established legal resources, Chapter 13 is a repayment plan lasting three to five years, designed for people with regular income who want to keep their property while catching up on what they owe.

Here is a quick overview of what each chapter involves:

- Chapter 7: Fast discharge, typically four to six months; non-exempt assets may be sold; ideal for lower-income filers with few significant assets

- Chapter 13: Three to five year repayment plan; you keep assets but commit to monthly payments; better suited for filers with regular income and property worth protecting

- Both chapters: Trigger the automatic stay, which immediately halts most collection actions, wage garnishments, and foreclosure proceedings when you file

- Both chapters: Available to individuals in Pennsylvania through the Eastern, Middle, or Western federal bankruptcy districts

"Chapter 7 moves relatively quickly—often within four to six months. For people who qualify, it can offer a clean financial reset without years of ongoing court obligations."

The contrast between these two paths shapes everything from how long you stay in the bankruptcy process to whether your home stays in your name. Understanding the starting point is essential before comparing details.

Key differences: Process, timeline, and property impact

Now that you know the basics, let's break down exactly how these options diverge in practice.

The most immediate difference is time. Chapter 7 typically concludes in four to six months. You file, the trustee reviews your case, a brief creditors' meeting occurs, and assuming no complications, your discharge follows. Chapter 13 requires three to five full years of court-supervised monthly payments before discharge is granted.

The second major difference involves what happens to your property. Under Chapter 7, the trustee can liquidate assets that fall outside Pennsylvania's exemptions. Under Chapter 13, you keep your property but must pay unsecured creditors at least the equivalent value of any non-exempt assets through your plan.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeline | 4 to 6 months | 3 to 5 years |

| Property risk | Non-exempt assets may be sold | Keep property; repay non-exempt value |

| Income requirement | Pass means test | Regular income required |

| Debt relief type | Discharge (no repayment) | Supervised repayment plan |

| Mortgage arrears | Not addressed through plan | Can be paid through plan |

| Best for | Low income, limited assets | Higher income, significant property |

Eligibility is another dividing line. Chapter 7 eligibility commonly depends on passing a means test tied to the debtor's income. If your average monthly income over the past six months exceeds Pennsylvania's median income for your household size, you may need to pass an additional expenditure calculation or consider Chapter 13 instead.

When it comes to real estate, the distinction becomes especially important. Chapter 13 allows repayment of missed mortgage payments through the plan, giving homeowners a structured way to stop foreclosure and get current. Chapter 7 does not provide that mechanism.

Here is a numbered breakdown of the key steps in each process:

- File a bankruptcy petition with the appropriate Pennsylvania federal district court

- Automatic stay activates, halting most creditor actions immediately

- Chapter 7: Trustee reviews assets and conducts a 341 meeting of creditors, typically within 30 to 40 days

- Chapter 13: Propose a repayment plan within 14 days; attend a confirmation hearing within 45 days

- Chapter 7: Receive discharge in roughly four to six months if no objections arise

- Chapter 13: Make monthly plan payments for three to five years, then receive discharge

Pro Tip: If you are behind on your mortgage in Pennsylvania, Chapter 13 is almost always the more protective option. It gives you a legal framework to cure arrears over time while keeping the lender from completing foreclosure, something Chapter 7 simply cannot replicate.

Working with an experienced bankruptcy attorney in Pennsylvania helps you navigate these procedural differences without stumbling into costly mistakes.

Who qualifies for Chapter 7 or Chapter 13 in Pennsylvania?

Understanding these choices raises the next question: which chapter are you actually eligible for in Pennsylvania?

Chapter 7 eligibility is determined primarily through the means test. This test compares your average household income over the past six months to Pennsylvania's median income for a comparable household. If your income falls below the median, you generally qualify automatically. If it exceeds the median, the test applies further calculations to determine whether you have enough "disposable income" after allowed expenses to repay creditors. Filers who fail the means test cannot use Chapter 7 and must consider Chapter 13 instead.

Chapter 13 eligibility carries its own requirements:

- You must have regular income, whether from employment, self-employment, Social Security, or another consistent source

- Your secured debt (such as mortgages and car loans) must fall below the applicable debt limits, which courts periodically adjust

- Your unsecured debt (such as credit cards and medical bills) must also remain within the statutory limit

- You must not have had a prior bankruptcy case dismissed within the past 180 days for certain specified reasons

- You must be willing and financially able to commit to three to five years of plan payments

"Even if you qualify for Chapter 7 based on income alone, your personal situation may make Chapter 13 the smarter legal strategy. Asset protection, mortgage arrears, and long-term financial goals all factor into that decision."

The role of assets adds a layer of complexity. Suppose you own a car with significant equity above Pennsylvania's exemption limits, or you are several months behind on your mortgage. Even if your income technically qualifies you for Chapter 7 eligibility in PA, filing Chapter 7 could put those assets at risk. In that scenario, Chapter 13 eligibility in PA may actually align better with protecting what you own.

Pennsylvania also allows filers to choose between state exemptions and federal exemptions, but you cannot mix and match. This choice significantly affects how much equity in a home, a vehicle, retirement accounts, or personal property you can protect.

Property and payments: How exemptions shape your path

With eligibility set, let's see how Pennsylvania's exemption laws can make or break what you keep and how much you pay.

Exemptions define what property the bankruptcy process cannot touch. Pennsylvania is one of the few states that allows filers to choose between the state's own exemption list and the federal bankruptcy exemptions. Because Pennsylvania's state exemptions are relatively limited in some categories, many filers choose the federal system.

Property treatment in Pennsylvania hinges directly on these exemptions. In Chapter 7, the trustee reviews all assets and can sell anything not protected by an exemption, using the proceeds to pay creditors. In Chapter 13, no assets are sold, but the plan must pay unsecured creditors at least the equivalent of the non-exempt equity the trustee could have recovered in a Chapter 7 case.

Here is how common Pennsylvania assets typically play out under each chapter:

| Asset type | Chapter 7 outcome | Chapter 13 outcome |

|---|---|---|

| Home with equity below exemption | Protected | Protected; no plan impact |

| Home with equity above exemption | Trustee may sell | Excess equity increases plan payment |

| Vehicle below exemption limit | Protected | Protected |

| Vehicle above exemption limit | Trustee may sell | Keep it; pay excess value through plan |

| Retirement accounts (401k, IRA) | Generally fully protected | Generally fully protected |

| Personal property above limit | At risk of liquidation | Pay equivalent value to creditors |

| Tax refunds received during case | May be taken by trustee | Often allocated to plan payment |

The distinction becomes especially important for sentimental or high-value personal property. A family heirloom, a second vehicle used by a teenager, or a modest recreational item can create complications in Chapter 7 if the value exceeds the available exemption.

Pro Tip: Sometimes paying into a Chapter 13 plan over three to five years is financially less costly than losing a non-exempt asset under Chapter 7. If you have a car worth $8,000 and the exemption only covers $3,500, Chapter 13 may let you keep it while paying the $4,500 gap through the plan rather than surrendering the car outright.

Success rates, risks, and real-life outcomes

Finally, success is not just the law's promise. It is the reality of finished plans and final discharges. Here is what Pennsylvanians really experience.

Chapter 7 carries a high completion rate. Once you file and meet basic requirements, the trustee's review proceeds and discharge follows in the vast majority of cases unless a creditor successfully objects or the trustee discovers hidden assets. Complications are relatively uncommon for straightforward consumer cases.

Chapter 13 tells a different story. Chapter 13 carries higher procedural risk, with many cases failing to reach discharge due to missed payments, life changes like job loss, or plan feasibility problems. Studies tracking nationwide outcomes show that only roughly 49.4% of Chapter 13 plans are completed successfully. For Pennsylvania filers, that number varies by district.

Chapter 13 outcomes are highly dependent on the federal judicial district and the quality of attorney execution. Pennsylvania has three federal bankruptcy districts, and each one carries its own judicial culture, trustee practices, and local rules that affect plan confirmation and completion rates.

What can you do to improve your odds? The following steps make a measurable difference:

- Hire an attorney with demonstrated local experience in your specific Pennsylvania federal district

- Build a realistic budget before filing so your plan payment is something you can genuinely sustain for three to five years

- Disclose all assets and income accurately from the start; omissions can lead to case dismissal or worse

- Stay current on post-filing obligations such as ongoing mortgage payments and tax returns

- Communicate early with your attorney if your financial situation changes during the plan; plan modifications are possible if pursued promptly

- Understand what happens if your plan fails: dismissal ends the automatic stay and restores creditors' full collection rights

The path to a bankruptcy fresh start in Pennsylvania is navigable, but it demands realistic planning and skilled legal support at every stage.

"A well-executed Chapter 13 plan, supported by an experienced local attorney, can actually outperform a rushed Chapter 7 filing in terms of long-term financial recovery."

Beyond the basics: What most guides miss about Chapter 7 vs. 13 in Pennsylvania

Most articles on this topic treat bankruptcy as a purely technical decision rooted in income thresholds and asset values. That framing is incomplete. In practice, the best chapter often comes down to factors that spreadsheets cannot capture: your personal stress tolerance, your willingness to live on a structured budget for years, and how much a specific asset matters to your daily life and sense of stability.

People who have gone through bankruptcy in Pennsylvania frequently describe the impact of their local attorney's knowledge as decisive, not just helpful. A trustee who regularly practices in the Western District of Pennsylvania may approach plan feasibility differently than one in the Eastern District. The right legal strategy for your situation accounts for those district-level patterns, not just the federal statutes.

Here is something most guides will not say outright: there is no universally "wrong" chapter. A person who qualifies for Chapter 7 but files Chapter 13 because they genuinely want to keep a home they love is not making an error. A person who could manage a Chapter 13 plan but prioritizes a clean, fast break and has no significant assets to protect is making a perfectly sound choice with Chapter 7. What matters is matching your specific financial reality, your goals, and your personal circumstances to the right legal tool.

The mistake is not choosing one chapter over the other. The mistake is choosing without understanding what you are actually agreeing to.

Pro Tip: Before committing to a filing strategy, interview at least two attorneys. Ask each one specifically about their outcomes in your district over the past two years. That question alone tells you more than any general comparison chart ever could.

Get guidance for your Pennsylvania bankruptcy decision

Choosing between Chapter 7 and Chapter 13 is a decision that affects your finances, your property, and your peace of mind for years. Reading guides like this one is a strong starting point, but personalized legal counsel translates that knowledge into an actual plan built around your income, assets, and goals.

At pennsylvaniadui.attorney, we connect Pennsylvania residents with experienced bankruptcy attorneys who know the local court landscape, the trustees, and the strategies that actually produce successful outcomes. Whether you are near Philadelphia, Pittsburgh, or anywhere in between, professional guidance turns a confusing process into a manageable one. Visit our Pennsylvania bankruptcy help page to explore your options, or reach out directly for North East bankruptcy support tailored to your region. A consultation costs you far less than a filing mistake.

Frequently asked questions

Which bankruptcy chapter is faster in Pennsylvania: Chapter 7 or 13?

Chapter 7 is significantly faster, typically concluding in four to six months, while Chapter 13 requires three to five years of court-supervised plan payments before a discharge is granted. For filers who qualify and have limited assets to protect, Chapter 7 offers a swift discharge without a lengthy repayment commitment.

Can I keep my house under Chapter 7 or Chapter 13?

If you are current on your mortgage and your home equity falls within exemption limits, Chapter 7 may let you keep it, but if you are behind on payments, Chapter 13 allows mortgage arrears to be repaid through the plan, making it the far stronger option for homeowners facing foreclosure.

What is the success rate for Chapter 13 bankruptcy in Pennsylvania?

Nationally, fewer than half of Chapter 13 cases end in a completed discharge, and Chapter 13 outcomes vary by district across Pennsylvania's three federal bankruptcy courts. Attorney experience and a realistic plan payment are the two strongest predictors of actually finishing the process successfully, as procedural and feasibility risks derail many filers.

What if I have valuable property that is not exempt?

In Chapter 7, a trustee can sell non-exempt property to pay creditors, but in Chapter 13, non-exempt property determines the minimum amount unsecured creditors must receive through your plan, allowing you to keep the asset while paying its equivalent value over time.