Bankruptcy is a federal legal process that allows qualified individuals to discharge or restructure debts by submitting a petition to the U.S. Bankruptcy Court under Title 11 of the United States Code. Knowing how to file bankruptcy correctly determines whether you walk away with a clean financial slate or face case dismissal. The two most common options for individuals are Chapter 7 liquidation and Chapter 13 reorganization, each with distinct eligibility rules and outcomes. Filing triggers an automatic stay that immediately halts wage garnishments, lawsuits, foreclosures, and collection calls. That protection begins the moment your petition hits the court clerk's desk, before any judge reviews your case.

How to file bankruptcy: Chapter 7 vs. Chapter 13 eligibility

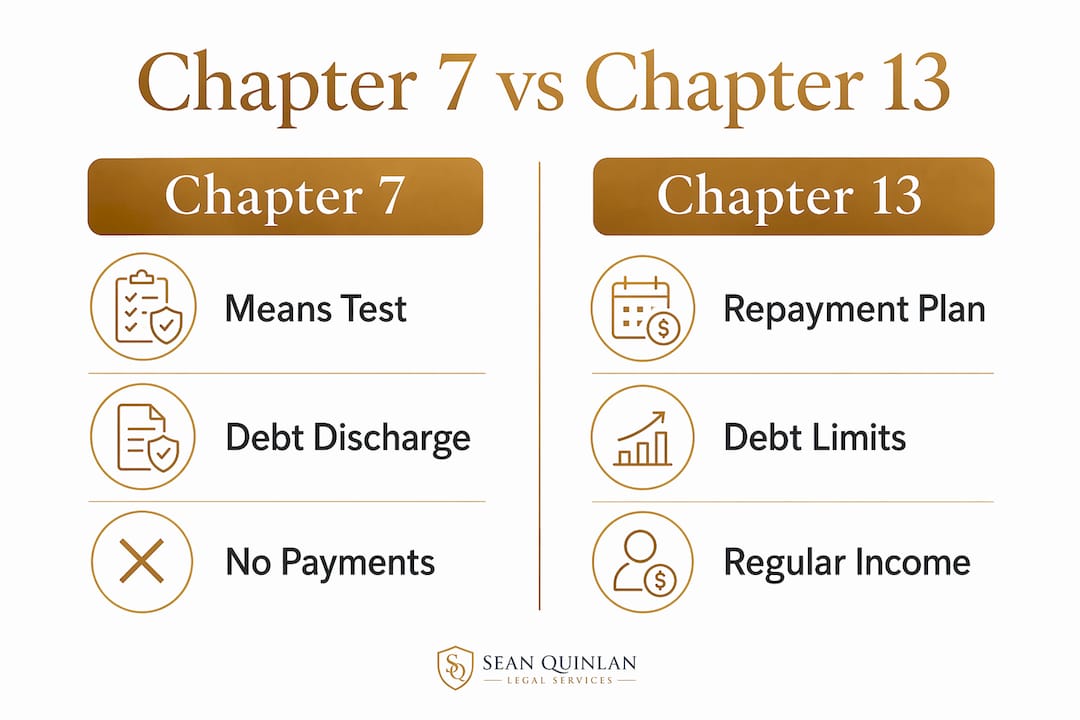

Choosing the right chapter starts with understanding the means test, which is the income-based formula courts use to determine Chapter 7 eligibility. If your current monthly income falls below Pennsylvania's median income for your household size, you pass automatically. If your income exceeds that threshold, you must complete a second calculation comparing your disposable income against allowable expenses. Failing the means test disqualifies you from Chapter 7 and typically redirects you toward Chapter 13.

Chapter 13 eligibility requires a regular income source and total secured and unsecured debts below the statutory limits set by federal law. You propose a repayment plan lasting three to five years, and creditors receive payments through a court-appointed trustee. This chapter works well for homeowners who want to stop foreclosure and catch up on mortgage arrears, or for filers with non-exempt assets they want to keep.

The table below compares the two chapters side by side to help you decide which path fits your situation.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Eligibility requirement | Must pass means test based on income | Must have regular income and meet debt limits |

| Timeline to discharge | 3 to 6 months from filing | 3 to 5 year repayment plan before discharge |

| Asset treatment | Non-exempt assets may be liquidated | Keep assets while repaying creditors |

| Best for | Unsecured debt, low income filers | Homeowners, filers with assets to protect |

| Filing fee (2026) | $338 | $313 |

For a deeper comparison tailored to Pennsylvania residents, Pennsylvaniadui has published a detailed breakdown of Chapter 7 vs. Chapter 13 options worth reviewing before you decide.

Pro Tip: Consult a bankruptcy attorney or a nonprofit credit counselor before choosing a chapter. A 30-minute consultation can prevent a costly filing mistake that takes years to undo.

What documents do you need to file bankruptcy?

Accurate, complete documentation is the foundation of a successful filing. Courts require full financial disclosure under penalty of perjury, meaning errors or omissions can result in dismissal or, in serious cases, fraud charges. Gathering everything before you start the official forms saves significant time and reduces the risk of mistakes.

Collect the following documents before completing any bankruptcy schedules:

- Two years of federal tax returns (or transcripts from the IRS if returns are unavailable)

- Six months of pay stubs or proof of all income sources, including self-employment records

- Bank statements for all accounts covering the past three to six months

- Titles and valuations for real estate, vehicles, and other significant assets

- A complete list of creditors with current balances, account numbers, and mailing addresses

- Monthly expense records including rent or mortgage, utilities, insurance, and food costs

- Loan and lease agreements for any secured debts

Once documents are gathered, you complete the official bankruptcy schedules and statements using forms from the U.S. Courts website at uscourts.gov. Key forms include Schedule A/B (assets), Schedule C (exemptions), Schedule D through F (creditors), Schedule I and J (income and expenses), and the Statement of Financial Affairs. The court requires detailed forms listing assets, debts, income, and expenses, all signed under penalty of perjury. That standard means every figure must be exact, not estimated.

Pro Tip: Make three copies of your complete filing packet before submitting. Keep one at home, bring one to the 341 meeting of creditors, and leave one with your attorney if you have one. Trustees frequently ask for documents you submitted weeks earlier.

If you need help organizing or notarizing documents, services like CF Legal Document Preparation offer DIY filing guides and document support for individuals preparing their own petitions.

Steps to file bankruptcy and handle court proceedings

The bankruptcy filing process follows a specific sequence. Skipping or mishandling any step can delay your discharge or get your case dismissed entirely.

-

Complete mandatory credit counseling. Federal law requires you to complete an approved credit counseling course within 180 days before filing. Pre-filing credit counseling and post-filing debtor education are both required steps before discharge is granted. Approved providers are listed on the U.S. Trustee Program website.

-

File your petition and pay the filing fee. Submit your completed petition, schedules, and statements to the bankruptcy court clerk in your district. The federal filing fee is $338 for Chapter 7 and $313 for Chapter 13 as of Q2 2026. Fee waivers are available for Chapter 7 filers whose income falls below 150% of the federal poverty line.

-

Receive your case number and automatic stay. The court assigns a case number immediately upon filing. The automatic stay takes effect at that moment, stopping all collection activity, foreclosure proceedings, and wage garnishments without any additional court order.

-

Attend the 341 meeting of creditors. Roughly 30 to 45 days after filing, you appear before the bankruptcy trustee at what is formally called the 341 meeting. Creditors may attend but rarely do in consumer cases. The trustee asks questions under oath about your finances and the accuracy of your filed documents. Most 341 meetings last under 10 minutes for straightforward cases.

-

Complete debtor education. After filing but before discharge, you must finish an approved personal financial management course. Failure to file the completion certificate with the court will prevent your discharge from being entered.

-

Receive your discharge. For Chapter 7, discharge typically occurs about 60 days after the 341 meeting, putting the total timeline at roughly three to six months. Chapter 13 discharge comes only after completing the full repayment plan, which spans three to five years.

Common mistakes that can derail your bankruptcy case

Certain actions taken before or during a bankruptcy filing can seriously damage your case. Courts and trustees are trained to identify financial behavior that suggests fraud or preferential treatment of certain creditors.

- Making preferential payments. Paying friends or certain creditors within one year before filing can be clawed back by the trustee and complicate your case significantly.

- Withdrawing retirement funds. Retirement accounts like 401(k)s and IRAs are generally fully protected in bankruptcy. Pulling those funds to pay debts before filing is one of the most common and costly mistakes filers make.

- Making luxury purchases or taking cash advances. Under 11 U.S.C. § 523(a)(2)(C), luxury purchases over $900 or cash advances over $1,250 shortly before filing are presumed fraudulent, making those debts nondischargeable.

- Omitting assets or creditors. Failing to list any asset or creditor, even one you believe is irrelevant, constitutes a false statement under penalty of perjury. Trustees cross-reference public records, tax filings, and credit reports.

- Ignoring waiting periods between filings. If you received a Chapter 7 discharge previously, you must wait eight years before filing Chapter 7 again. Filing too soon results in automatic ineligibility.

Fraudulent transfers and luxury purchases before filing can jeopardize discharge and lead to legal penalties. The safest rule: make no unusual financial moves in the months before you file without first speaking to an attorney.

Can you file bankruptcy without a lawyer?

Federal law under 28 U.S.C. § 1654 grants every individual the right to represent themselves, known as pro se filing, in bankruptcy court. Whether that right is practical depends heavily on which chapter you file and how complex your financial situation is.

For Chapter 7, pro se filing is viable in straightforward cases. Approximately 8 to 10% of Chapter 7 cases are filed without attorney representation, and many succeed when the filer has limited assets, no business interests, and primarily unsecured debt. The forms are detailed but follow a logical structure, and resources like the U.S. Courts self-help center and legal aid organizations can fill gaps.

Chapter 13 is a different story. Chapter 13 self-filing often results in dismissal because the repayment plan must satisfy specific legal standards, and trustees and creditors actively challenge plans that do not comply. The procedural complexity alone makes professional help strongly advisable.

Consider these factors when deciding whether to hire an attorney:

- Case complexity: Multiple properties, business debts, or disputed creditor claims all favor attorney involvement.

- Cost vs. risk: Pro se total costs including credit counseling typically range between $370 and $440. Attorney fees for Chapter 7 in Pennsylvania commonly range from $1,000 to $1,500. The cost difference narrows when you factor in the risk of dismissal.

- Available resources: Legal aid organizations in Pennsylvania, including Community Legal Services in Philadelphia and MidPenn Legal Services, offer free or reduced-cost bankruptcy help for qualifying individuals.

Pro Tip: Most bankruptcy attorneys offer free initial consultations. Use that meeting to assess whether your case is simple enough for pro se filing or complex enough to justify legal fees. You are not obligated to hire anyone after a consultation.

For Pennsylvania-specific guidance on the Chapter 7 process, Pennsylvaniadui's Chapter 7 relief guide covers exemptions and local court procedures in detail.

Key takeaways

Filing bankruptcy successfully requires choosing the right chapter, completing mandatory counseling, and avoiding financial missteps before and during the process.

| Point | Details |

|---|---|

| Choose the right chapter | Chapter 7 suits low-income filers; Chapter 13 protects assets and stops foreclosure. |

| Automatic stay is immediate | Filing halts all collections, garnishments, and foreclosures the moment the petition is submitted. |

| Documentation must be exact | All schedules are signed under penalty of perjury; errors or omissions can cause dismissal. |

| Avoid pre-filing mistakes | Do not make preferential payments, withdraw retirement funds, or make luxury purchases before filing. |

| Pro se works for simple Chapter 7 | Self-representation is viable for straightforward cases but carries high dismissal risk in Chapter 13. |

What I've learned from watching clients wait too long to file

Many individuals treat bankruptcy as a last resort, something to pursue only after every other option has failed. That instinct is understandable, but it often leads to worse outcomes. By the time some clients come to me, they have already drained retirement accounts, made large payments to family members, or taken cash advances trying to stay afloat. Each of those actions creates a legal problem inside the bankruptcy case that would not have existed if they had filed six months earlier.

The misconception I encounter most often is the belief that bankruptcy means losing everything. For most Pennsylvania filers, that is simply not true. State and federal exemptions protect a primary residence up to a certain equity threshold, one vehicle, household goods, and retirement accounts entirely. The fear of asset loss keeps people in financial paralysis far longer than necessary.

Student loans are a genuine limitation worth addressing honestly. Student loans generally survive bankruptcy unless discharged through a separate adversary proceeding proving undue hardship, which is a high legal bar. If student debt is your primary problem, bankruptcy may not be the right tool on its own. But if student loans are one piece of a larger debt picture, bankruptcy can eliminate the surrounding debt and free up cash flow to manage loan payments.

My honest advice: treat bankruptcy as a strategic legal tool, not a sign of failure. The federal system designed it specifically to give people a genuine fresh start. Using it at the right time, with full disclosure and proper preparation, is exactly what it was built for.

— Sean

Get professional bankruptcy help in Pennsylvania

Facing the bankruptcy filing process alone is possible in simple cases, but the stakes are high enough that professional guidance makes a measurable difference in outcomes.

Attorney Sean Quinlan at Pennsylvaniadui provides personalized bankruptcy representation for Pennsylvania residents, covering both Chapter 7 and Chapter 13 filings across multiple counties. From the initial means test analysis through the 341 meeting and discharge, the focus is on protecting your rights, preserving your exempt assets, and getting your case resolved correctly the first time. If you are ready to take the next step, visit the bankruptcy services page to schedule a consultation and get a clear picture of your options.

FAQ

What is the first step to file bankruptcy?

The first step is completing an approved credit counseling course within 180 days before filing. After that, you gather financial documents and complete the official bankruptcy petition and schedules through the U.S. Courts website.

How long does bankruptcy take to discharge debt?

Chapter 7 discharge typically occurs about 60 days after the 341 meeting of creditors, putting the total process at three to six months. Chapter 13 requires completing a three to five year repayment plan before discharge is granted.

How do you qualify for Chapter 7 bankruptcy?

You must pass the means test, which compares your current monthly income to Pennsylvania's median income for your household size. If your income exceeds the median, a second calculation determines whether your disposable income is low enough to qualify.

What should you not do before filing bankruptcy?

Avoid making large payments to friends or family, withdrawing retirement funds, making luxury purchases over $900, or taking cash advances over $1,250 shortly before filing. These actions can be treated as fraudulent and may make certain debts nondischargeable.

Can bankruptcy stop a wage garnishment immediately?

Yes. Filing a bankruptcy petition triggers an automatic stay that halts wage garnishments, foreclosures, lawsuits, and collection calls the moment the petition is submitted to the court, before any hearing takes place.