If you are facing serious debt pressure and considering bankruptcy, understanding what is bankruptcy counseling may be the most important step you take before anything else. This is not an optional class or a suggestion from your attorney. Federal law requires most individuals to complete specific counseling courses before and after filing, and skipping either one can result in your case being dismissed. This article explains exactly what these courses involve, how the bankruptcy counseling process works from start to finish, what benefits the process offers, and how to avoid the common mistakes that derail many filings.

Table of Contents

- Key takeaways

- What is bankruptcy counseling and its legal requirements

- How the bankruptcy counseling process works

- Benefits of bankruptcy counseling and available alternatives

- Common pitfalls in bankruptcy counseling

- Applying this knowledge to your financial decisions

- My honest take on bankruptcy counseling

- How Attorney Sean Quinlan can guide you through the process

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Two courses are required | Credit counseling happens before filing; debtor education happens after filing. These are separate sessions. |

| Strict timing rules apply | Pre-filing credit counseling must be completed within 180 days before you file or your case can be dismissed. |

| Only approved providers count | Courts only accept certificates from providers authorized by the U.S. Trustee Program. |

| Counseling reveals alternatives | A counselor may present a debt management plan that avoids bankruptcy entirely. |

| Certificates must be filed | You must submit completed course certificates to the court as part of your bankruptcy documentation. |

What is bankruptcy counseling and its legal requirements

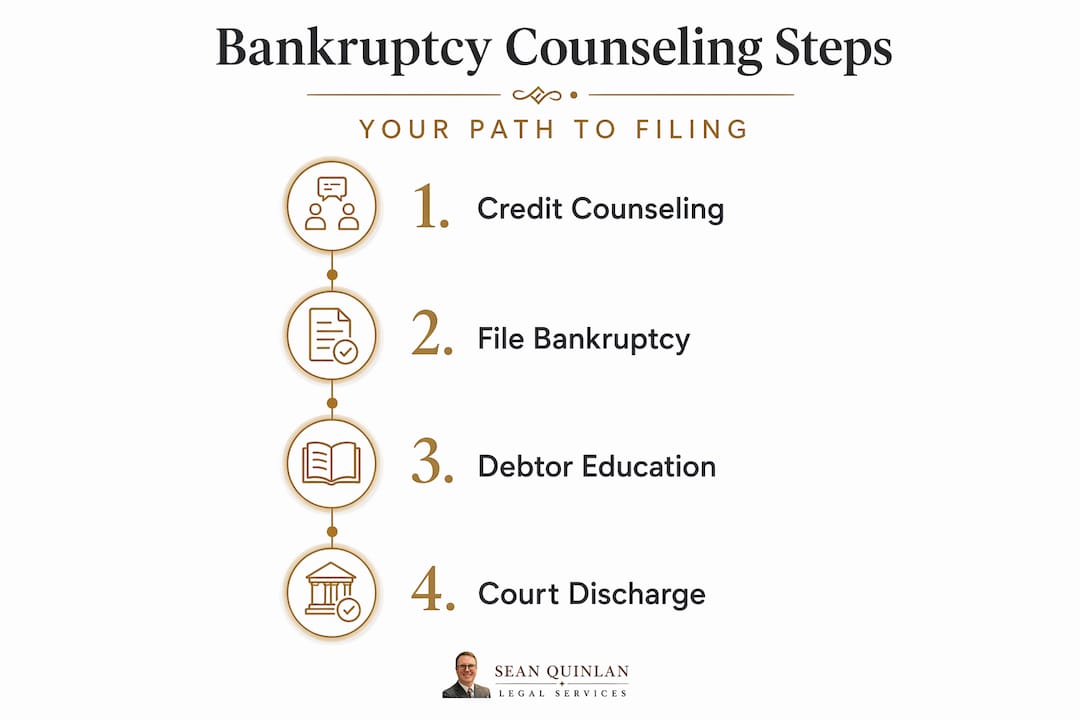

Bankruptcy counseling is a federally mandated educational process that consists of two separate courses. The first course is credit counseling, completed before you file your bankruptcy petition. The second is debtor education, completed after you file but before your debts are discharged. Both courses are required under the Bankruptcy Abuse Prevention and Consumer Protection Act of 2005 for most personal bankruptcy filings, including Chapter 7 and Chapter 13 cases.

These two sessions serve distinct purposes and cannot be substituted for each other. Credit counseling focuses on reviewing your financial situation and exploring whether alternatives to bankruptcy exist. Debtor education focuses on money management skills that will help you avoid future financial trouble. Confusing them or completing them out of order creates procedural problems that can complicate your filing.

Here is what the legal requirements specifically demand:

- Pre-filing credit counseling: Must be completed within 180 days before filing your bankruptcy petition. Completing it a day outside that window means the certificate is invalid.

- Approved providers only: The court will only accept certificates from agencies authorized by the U.S. Trustee Program. Not every nonprofit credit counseling agency qualifies.

- Debtor education after filing: This course must be finished after you file but before the court enters your discharge order.

- Certificate submission: Both certificates must be filed with the bankruptcy court as official documents in your case.

Pro Tip: Before registering for any counseling course, visit the U.S. Trustee Program's official website and confirm that your chosen provider is on the approved list for your judicial district. An unapproved course is money and time wasted.

How the bankruptcy counseling process works

Understanding how does bankruptcy counseling work in practice removes much of the anxiety surrounding it. The process is straightforward once you know the steps.

-

Locate an approved provider. Search the U.S. Trustee Program's database to find approved counseling agencies in your district. Different providers may be required for credit counseling versus debtor education, so check both lists carefully before enrolling.

-

Choose your format. Most approved providers offer three delivery formats: online, by phone, or in person. Online courses are the most commonly used option because of convenience, and many providers allow you to complete them at any hour.

-

Complete the credit counseling session. Expect to spend roughly 60 to 90 minutes on the pre-filing course. Sessions cover your current income, expenses, debts, and potential alternatives to bankruptcy such as negotiation or a debt management plan. Fees typically range from $10 to $50, and fee waivers are available for those who qualify based on income.

-

Receive your certificate. After completing the course, the agency issues a certificate of completion. This document has an expiration tied to the 180-day window, so your filing date must fall within that period.

-

File your bankruptcy petition. With your credit counseling certificate in hand, you can now formally file your case with the bankruptcy court.

-

Complete the debtor education course. After filing, you must complete a separate financial management course. Credit counseling agencies that are nonprofit organizations typically offer this course as well, though again, verify provider approval.

-

Submit the debtor education certificate. File this second certificate with the court. Without it, the court will not issue a discharge of your debts, which is the entire goal of the bankruptcy process.

Pro Tip: Do not complete your credit counseling course too early. If there is any chance your filing date will slip due to document gathering or attorney scheduling, take the course closer to your intended filing date to protect the 180-day validity window.

Benefits of bankruptcy counseling and available alternatives

The importance of bankruptcy counseling goes well beyond satisfying a legal checkbox. There are real, practical benefits to engaging with the process honestly.

One of the most significant benefits is the possibility of avoiding bankruptcy altogether. Debt management plans offered through credit counseling agencies can reduce interest rates and spread payments over three to five years, making debts manageable without the long-term credit consequences of a bankruptcy filing. Not everyone qualifies, but many people who walk in planning to file walk out with a workable repayment plan instead.

Beyond the debt management option, the counseling session forces you to sit down and get a complete, honest picture of your finances. Many people arrive with a vague sense of being overwhelmed. The counselor works through your specific income, expenses, and debt load in a structured way. That clarity alone has value.

- Informed decision-making: You will understand exactly how much debt you carry, what your repayment options are, and what bankruptcy will actually accomplish for your situation.

- Potential payment negotiations: Some agencies can help open communication with creditors to negotiate better terms before a formal filing.

- Financial education: The debtor education course gives you money management tools that reduce the likelihood of returning to serious debt.

- Documentation for court: Completing both courses correctly gives your attorney clean paperwork to work with, reducing delays.

Bankruptcy counseling aims to ensure that debtors understand all available options before filing, preventing rushed filings made without full knowledge of alternatives or obligations.

Even if counseling confirms that bankruptcy is the right path, you will enter the process with a clearer understanding of what comes next. That preparation matters.

Common pitfalls in bankruptcy counseling

Many filers run into problems not because of the complexity of the courses themselves but because of misunderstanding the rules around them. Here is a direct comparison of the two required courses to show how distinct they are:

| Feature | Credit counseling | Debtor education |

|---|---|---|

| When completed | Before filing | After filing |

| Primary focus | Financial review and alternatives | Money management and budgeting |

| Typical duration | 60 to 90 minutes | About 2 hours |

| Certificate validity | 180 days before filing date | Must be filed before discharge |

| Provider requirement | U.S. Trustee approved | U.S. Trustee approved (may differ) |

The most common mistake is treating these as interchangeable. They are not. Completing both courses before filing, for example, does not satisfy the debtor education requirement. The court requires the second course to occur after the petition is filed.

Timing errors are the next most frequent problem. The 180-day certificate window is treated as a hard deadline by the courts. A certificate completed on day 181 is invalid. If your case gets delayed and your certificate expires, you will need to retake the course and pay again.

Provider selection errors also cause trouble. Picking a provider not approved by the U.S. Trustee Program means the court will not recognize your certificate. Some providers handle both courses while others only offer one. Assuming your credit counseling agency automatically qualifies to provide debtor education is a mistake that can delay your discharge.

Applying this knowledge to your financial decisions

Knowing the rules gives you a significant advantage. Here is how to use what you have learned to move forward with confidence:

- Evaluate the counselor's recommendations seriously. If the session reveals a workable debt management plan, consider it honestly before committing to filing. Some individuals save themselves years of credit damage this way.

- Plan your counseling date around your intended filing date. Work backward from when you expect to file and schedule your credit counseling session with enough lead time, but not so early that the 180-day window closes before you file.

- Keep all documentation organized. Store your certificates digitally and in print. Your attorney will need them, and the court requires them as part of the official record.

- Consult a qualified bankruptcy attorney. A skilled attorney can review your certificates, confirm provider approval status, and make sure both courses are timed correctly relative to your petition date. Learn more about how a bankruptcy attorney protects your financial future in Pennsylvania.

- View the process as a starting point. Completing bankruptcy counseling is not just a procedural hurdle. It is the beginning of a structured path toward resolving debt and regaining financial footing.

The bankruptcy counseling process, done correctly, positions you to get the most out of your filing while avoiding the procedural errors that cause otherwise valid cases to stall.

My honest take on bankruptcy counseling

I have worked with enough clients navigating bankruptcy to say this plainly: the people who treat counseling as an obstacle are the ones who show up to the filing process least prepared. The ones who engage with it genuinely are the ones who come out the other side with a real understanding of their finances.

What I have seen repeatedly is that clients rush to file without fully absorbing what the counselor presents. They want relief, and they want it fast. I get it. But the session often contains real information about their financial picture that changes the calculus, whether it confirms bankruptcy is the right call or reveals a path they had not considered.

I have also seen filings delayed by something as avoidable as a certificate that expired by two weeks. The 180-day window sounds generous until life intervenes and document gathering takes longer than expected. My advice is always to time the counseling session about two to three weeks before your intended filing date, not six months out.

One misconception I encounter often is the belief that any nonprofit financial counseling counts. It does not. The U.S. Trustee Program approval requirement is non-negotiable, and courts do not make exceptions. Verifying your provider before you pay and complete the course takes five minutes and prevents significant frustration. Treat the certificate as the legal document it is. File it properly, protect it, and make sure your attorney has a copy well before your hearing date.

— Sean

How Attorney Sean Quinlan can guide you through the process

Facing bankruptcy is stressful enough without having to decode federal counseling requirements on your own. At Pennsylvaniadui, Attorney Sean Quinlan works directly with individuals across Pennsylvania to make sure every step of the bankruptcy counseling process is handled correctly, from identifying approved providers to meeting the strict timing requirements for certificate submission.

Sean understands that missing a deadline or selecting the wrong provider can derail an otherwise straightforward case. That is why the firm provides hands-on guidance for each client, reviewing documentation, confirming compliance, and managing filings with the court. Whether you are just beginning to explore your options or you are ready to file, getting qualified legal support early makes a real difference.

If you are ready to take the first step toward a fresh financial start, visit the bankruptcy services page to schedule a consultation with Attorney Sean Quinlan today. For residents in the Bellwood area, local bankruptcy assistance is also available with the same personalized approach.

FAQ

What is bankruptcy counseling required for?

Bankruptcy counseling is legally required for most individuals filing Chapter 7 or Chapter 13 bankruptcy. Federal law mandates both a pre-filing credit counseling session and a post-filing debtor education course before debts can be discharged.

How long does bankruptcy counseling take?

The pre-filing credit counseling course typically takes 60 to 90 minutes and costs between $10 and $50. The post-filing debtor education course usually runs about two hours.

What happens if I miss the 180-day counseling deadline?

If your credit counseling certificate was issued more than 180 days before your filing date, the certificate is invalid and your case can be dismissed. You would need to retake the course within the required window.

Can bankruptcy counseling help me avoid filing?

Yes. A counselor may present a debt management plan that reduces interest and extends payments over three to five years, which may resolve your debt without the need to file for bankruptcy.

Where can I find approved bankruptcy counseling providers?

Approved providers are listed in the U.S. Trustee Program database, which is organized by judicial district. Courts only accept certificates from authorized agencies on that list.