After a car accident in Pennsylvania, most people receive an insurance offer that sounds reasonable until they realize it may cover only a fraction of what they actually lost. Insurer formulas undervalue claims routinely, and attorney negotiation often doubles initial offers when supported by strong evidence. Understanding how compensation is actually calculated gives you the knowledge to push back, negotiate with confidence, and protect your financial recovery from start to finish.

Table of Contents

- Essential requirements for accident compensation calculations

- Step-by-step process to calculate compensation

- Common pitfalls and how to avoid them

- What to expect after calculating your compensation

- Why most people settle for less (and how Pennsylvania makes it tricky)

- Get expert help maximizing your accident compensation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Gather thorough documentation | Collect every bill, wage record, and accident detail to start your compensation calculation on solid ground. |

| Understand Pennsylvania rules | Your claim value depends strongly on local laws, especially Limited vs. Full Tort choices. |

| Apply both major formulas | Use the multiplier and per diem methods for a realistic compensation estimate. |

| Beware common mistakes | Don't settle for low offers or overlook details that can drastically lower your settlement. |

| Negotiation often raises offers | Attorney-supported negotiation with strong evidence can double settlement payouts. |

Essential requirements for accident compensation calculations

Now that you see why most offers are low, start by preparing essential paperwork and understanding local rules before you calculate anything.

Getting your compensation number right starts with gathering the right information. Missing even one key document can cause you to underestimate your claim or accept less than you deserve. Here is what you need to collect before running any numbers:

- Medical records and bills: Every hospital visit, emergency room charge, specialist appointment, prescription, physical therapy session, and future treatment estimate should be documented in writing.

- Lost wages documentation: Pay stubs, employer letters, tax returns, and time-off records confirm what you could not earn while recovering.

- Insurance policy details: Knowing whether you carry Full Tort or Limited Tort coverage is critical before you calculate anything. More on this below.

- Evidence of fault: Police reports, witness statements, traffic camera footage, and photos from the scene establish who caused the accident.

- Pain and suffering records: A daily journal describing your physical pain, emotional distress, and limitations on daily life is powerful supporting evidence.

One of the most important Pennsylvania-specific factors is the tort election on your auto insurance policy.

| Coverage type | What you can claim | Premium impact |

|---|---|---|

| Full Tort | All damages, including pain and suffering | Higher premium |

| Limited Tort | Only economic losses unless injury is "serious" | ~15% lower premium |

Important: The Limited Tort trap catches many Pennsylvania drivers off guard. Choosing it may save roughly 15% on premiums but can cost you 10 times or more in a real claim by blocking recovery for pain and suffering unless your injury meets a high legal threshold.

Pennsylvania defines a "serious injury" under Limited Tort as death, serious impairment of a body function, or permanent serious disfigurement. Soft tissue injuries, whiplash, and other common accident injuries may not qualify. This means that if you chose Limited Tort when setting up your policy, you might be entitled to far less than someone with identical injuries under Full Tort coverage.

Understanding these injury terms explained in Pennsylvania law helps you assess your claim accurately from the start. You cannot negotiate effectively if you do not know what category of damages you are legally permitted to pursue.

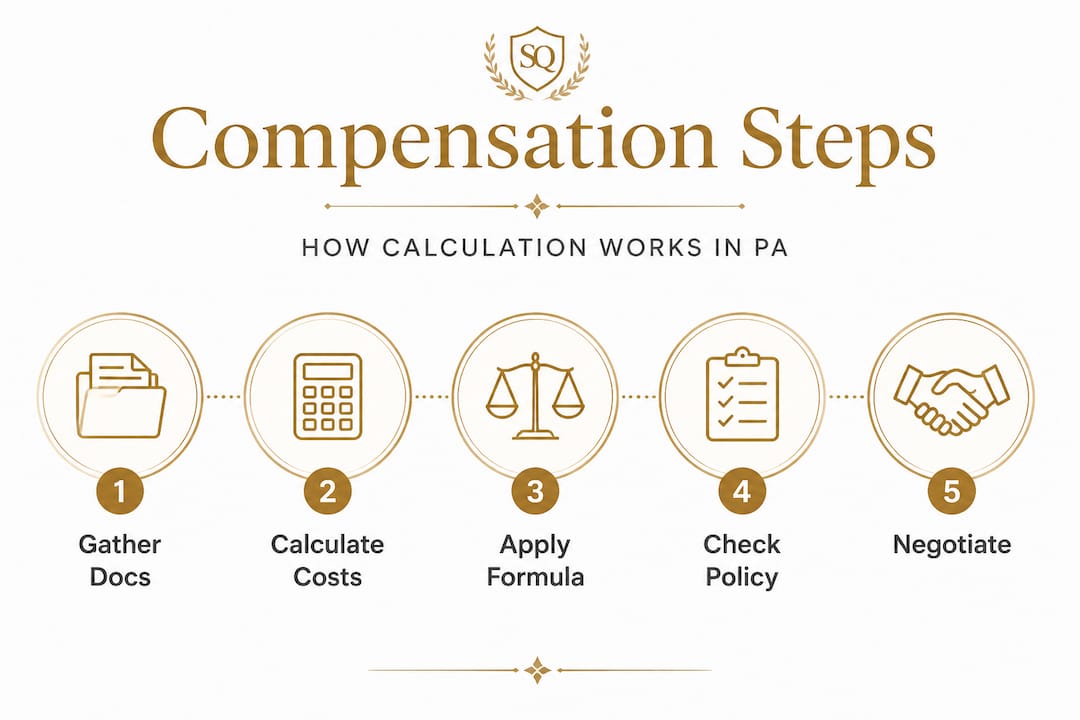

Step-by-step process to calculate compensation

With your documents and key terms ready, you are set to follow each calculation step and see where real claim values come from.

There are two widely used methods for calculating accident compensation in personal injury cases. Neither one is a guarantee of what you will receive, but both serve as important starting points for any negotiation.

Method 1: The multiplier method

- Add up all economic losses. This includes medical bills (past and projected), lost wages, property damage, and other out-of-pocket costs. For example, if your total economic losses are $25,000, that is your base figure.

- Assign a multiplier based on injury severity. Multipliers typically range from 1.5 for minor injuries to 5 or higher for catastrophic or permanent injuries. A moderate injury with significant recovery time might earn a multiplier of 2.5 to 3.

- Multiply economic losses by the chosen multiplier. Using $25,000 at a multiplier of 3 gives a starting claim value of $75,000.

- Add any non-economic losses not already captured. If you have specific evidence of emotional distress or long-term lifestyle limitations, document those separately.

Method 2: The per diem method

- Assign a daily dollar value to your pain and suffering. Many attorneys use your daily wage as a reasonable benchmark. If you earn $200 per day, that becomes your per diem rate.

- Count the number of days you experienced significant pain. This might be 90 days of acute recovery or 365 days if you have a chronic condition.

- Multiply the daily rate by the number of days. At $200 per day for 180 days, your pain and suffering value equals $36,000.

- Add this figure to your total economic losses for a combined compensation estimate.

| Method | Best used when | Typical range |

|---|---|---|

| Multiplier | Serious injuries with high medical costs | 1.5x to 5x economic damages |

| Per diem | Injuries with a clear recovery timeline | Daily rate x recovery days |

| Insurer's offer | Starting negotiation point only | Often below both formulas |

The critical reality is that insurers routinely lowball both formulas, using their own internal models designed to minimize payouts. Attorney negotiation backed by solid evidence frequently doubles initial offers.

To maximize your compensation, you need to document aggressively, present your evidence systematically, and treat every insurer communication as part of a negotiation, not a friendly conversation.

Pro Tip: Never accept the first offer from an insurer without running your own numbers using both formulas. If the offer is significantly below your estimate, that gap is your negotiation room. Gather every additional piece of evidence you can and be prepared to pursue compensation claims through formal legal channels if needed.

Common pitfalls and how to avoid them

Even with a solid calculation, mistakes or traps can keep you from getting what you deserve. Pennsylvania has a few specific traps that catch accident victims more than almost any other aspect of the claims process.

Undervaluing pain and suffering: Many people feel uncomfortable assigning a dollar figure to emotional distress or chronic pain, so they accept whatever number the insurer provides. Do not make this mistake. Pennsylvania law allows recovery for physical pain, mental anguish, lost enjoyment of life, and disfigurement. Each of these is real and compensable.

Assuming the first offer is final: Insurers present initial offers with confidence because they know many claimants accept them without question. The first offer is almost never the best offer. Treat it as an opening position.

Ignoring future medical costs: If your injury requires ongoing treatment, surgery, or therapy in the future, those costs belong in your calculation today. Failing to include projected future expenses is one of the most common reasons settlements fall short.

Missing deadlines: Pennsylvania's statute of limitations for personal injury claims is generally two years from the date of the accident. Miss that deadline, and you may lose your right to any compensation, regardless of how strong your case is.

Losing or failing to preserve evidence: Photographs fade from memory, witnesses become unavailable, and surveillance footage gets overwritten. Preserve everything as quickly as possible after an accident.

The Limited Tort warning again: Research confirms the Limited Tort premium saving of roughly 15% can cost you many times that amount in a serious claim. Before you assume your policy allows you to claim pain and suffering, verify your tort election in writing.

Understanding your accident rights in PA before you begin negotiating helps you avoid surrendering rights you did not know you had. Similarly, reviewing your personal injury rights in PA ensures you understand what compensation categories are legally available to you.

Pro Tip: If any detail of your claim is unclear, including your tort status, the at-fault determination, or a disputed medical bill, consult a legal professional before responding to any insurer communication. A single poorly worded statement can compromise your claim.

What to expect after calculating your compensation

Avoiding mistakes means you can use your calculation effectively. Here is what the process typically looks like after you have your number in hand.

Your calculation is a negotiation tool, not a payment guarantee. Understanding this distinction is important. Once you present your demand, the insurer will respond with a counteroffer, a request for additional documentation, or a denial. Each of these responses is a step in a process, not a verdict.

- Submit a formal demand letter. Include your total calculation, supporting evidence, and a clear statement of what you are requesting. A well-organized demand letter signals to the insurer that you understand your claim's value.

- Evaluate the counteroffer carefully. Compare the insurer's number against your documented losses. Identify which categories they discounted and why. This tells you where to focus your rebuttal.

- Provide additional evidence if needed. Updated medical records, a second physician opinion, or a vocational expert's assessment of lost earning capacity can all strengthen your position significantly.

- Know when to escalate. If the insurer refuses to negotiate in good faith or continues to offer a figure that does not reflect your actual losses, legal representation becomes necessary.

By the numbers: Evidence shows that attorney negotiation doubles offers when backed by medical documentation, expert testimony, and a clear liability record. This is not an accident. Attorneys understand insurer tactics and know which arguments move the needle.

The next steps after an accident matter enormously for how much leverage you carry into any negotiation. Claimants who document thoroughly, act quickly, and respond strategically to insurer communications consistently achieve better outcomes than those who accept early offers without review.

Knowing your calculated number before any negotiation gives you something priceless: a factual foundation to stand on. You are no longer guessing what your claim is worth. You have a documented, evidence-based figure that you can defend point by point.

Why most people settle for less (and how Pennsylvania makes it tricky)

Pennsylvania's dual tort system creates a level of confusion that works systematically against accident victims who have not done their homework. Most people choose Limited Tort without fully understanding what they are giving up. When the accident happens, they discover the hard way that their policy bars them from recovering pain and suffering compensation. That gap between expectation and reality is where the real financial damage occurs.

Insurers understand this confusion deeply. Their adjusters are trained to move quickly, establish rapport, and present an offer before the claimant has time to consult an attorney or calculate their actual losses. Time pressure is one of the most effective tools in an insurer's playbook. When you are dealing with medical bills, missed work, and physical pain, a check that arrives fast can feel like relief even when it is far below what you deserve.

The Limited Tort premium saving of 15% sounds reasonable when you are setting up a policy. But when you are sitting across from an adjuster after a serious accident, that 15% premium savings can cost you tens of thousands of dollars in legitimate compensation you simply cannot access.

What do successful claimants do differently? They prepare before they negotiate. They understand their tort status, gather every piece of supporting documentation, and run their own numbers using the multiplier and per diem methods. They treat the insurer's first offer as a starting point and respond with a documented counteroffer, not silence or immediate acceptance.

They also recognize when to bring in professional help. An experienced Pennsylvania personal injury attorney does not just negotiate. The attorney understands how to read insurer settlement authority, frame medical evidence compellingly, and apply legal pressure at the right moments. That combination of legal knowledge and negotiation skill is precisely why represented claimants consistently recover more than unrepresented ones.

Following essential protection steps immediately after your accident preserves the evidence and documentation that make every subsequent step more effective. The claimants who do this well are not necessarily the ones with the most severe injuries. They are the ones who treated their claim like the serious legal matter it actually is.

Get expert help maximizing your accident compensation

Calculating your compensation is a powerful first step, but knowing your number and recovering that number are two very different things. Insurers have experienced adjusters, legal teams, and internal models designed to minimize what they pay. Going into that process without professional support puts you at a real disadvantage.

At Pennsylvania DUI Attorney, we work with accident victims across Pennsylvania to evaluate claims, challenge low insurer offers, and build the evidence-based case that gets results. Whether you need guidance on your calculation or full representation through a dispute, our team is ready to help. If you have been in an auto accident, start with our get auto accident help page, or if you are dealing with broader injury losses, connect with us to consult a personal injury attorney who understands the Pennsylvania landscape. A better settlement is often closer than you think.

Frequently asked questions

What documents do I need to calculate accident compensation?

You will need medical bills, proof of lost wages, your insurance policy details, and any written or photographic evidence of pain, injury, and long-term effects on your daily life.

What's the difference between Full Tort and Limited Tort in Pennsylvania?

Full Tort allows you to claim all damages including pain and suffering, while Limited Tort saves roughly 15% on premiums but typically blocks pain and suffering recovery unless your injury qualifies as legally "serious."

How accurate are online accident compensation calculators?

They provide a useful starting estimate based on standard formulas, but insurer lowballing tactics and attorney negotiation backed by evidence often change the final settlement amount significantly.

Can I increase my settlement after an offer?

Yes. Presenting additional medical evidence or working with a qualified attorney can often double the initial offer an insurer puts on the table in Pennsylvania personal injury cases.