A bankruptcy petition is the formal legal document filed with a federal bankruptcy court to officially initiate a bankruptcy case and trigger the automatic stay, which immediately halts most creditor collection actions. Filing this document is the single act that places you under court protection, stopping wage garnishments, foreclosures, and creditor calls from that moment forward. For residents of Camp Hill, Harrisburg, Cumberland County, and Dauphin County, understanding the petition process is the first step toward regaining financial control. The filing fees in 2026 are $338 for Chapter 7 and $313 for Chapter 13, making the cost of entry relatively modest compared to the relief it can provide.

What is a bankruptcy petition and what does it contain?

A bankruptcy petition is the gateway document that formally opens your case before the U.S. Bankruptcy Court. It is not a single page. It is a package of forms, schedules, and supporting documents that paint a complete picture of your financial life.

The core components of a standard individual petition include:

- Personal identification data: Your legal name, address, Social Security number, and prior addresses from the last three years

- Chapter selection: A declaration of which chapter you are filing under, such as Chapter 7 or Chapter 13

- Asset schedules: A detailed inventory of everything you own, including real estate, vehicles, bank accounts, and personal property

- Liability schedules: A complete list of every debt you owe, including creditor names, account numbers, and balances

- Income and expense statements: Monthly income from all sources and a breakdown of living expenses

- Statement of Financial Affairs: A history of recent financial transactions, including transfers, payments to creditors, and lawsuits

- Credit counseling certificate: Proof that you completed the mandatory pre-filing counseling course

The primary form for individual filers is Official Form 101, the Voluntary Petition for Individuals Filing for Bankruptcy. Chapter 13 petitions require additional documentation because they include a proposed repayment plan, which makes the filing package considerably more detailed than a Chapter 7 filing.

Bankruptcy fraud carries severe penalties, including fines up to $250,000 and imprisonment for up to five years under 18 U.S.C. § 152. Because petition signatures are made under penalty of perjury, every figure must be exact. Inaccuracies on petition forms may lead to denial of discharge or loss of exemptions, not just minor corrections.

Pro Tip: Never round figures or estimate asset values on your petition. The trustee assigned to your case will compare your disclosures against tax returns, bank statements, and public records. Even a small discrepancy on a minor asset can trigger scrutiny of your entire filing.

How to file a bankruptcy petition in Central Pennsylvania

The federal bankruptcy court serving Harrisburg, Camp Hill, Cumberland County, and Dauphin County is the U.S. Bankruptcy Court for the Middle District of Pennsylvania. York County residents also fall within this district. Filing in the correct district is a threshold requirement. Filing in the wrong court results in dismissal.

Here is the step-by-step process for filing your petition:

- Complete the mandatory credit counseling course. Pre-filing credit counseling must be completed within 180 days before filing. The course takes 60 to 90 minutes and costs between $15 and $50 from an approved provider. You will receive a certificate that must be filed with your petition.

- Gather all financial documents. Collect two years of tax returns, six months of pay stubs, bank statements, mortgage statements, vehicle titles, and a complete list of creditors with current balances.

- Complete all required forms. Use the official bankruptcy forms available through the U.S. Courts website. Individual filers use Official Form 101 along with the full suite of schedules A through J.

- Pay the filing fee or request a waiver. The 2026 fee is $338 for Chapter 7 and $313 for Chapter 13. Low-income filers may qualify for a fee waiver or installment payment arrangement by submitting Official Form 103A or 103B.

- Submit your petition. Attorneys file electronically through the court's CM/ECF system. Pro se filers, meaning those representing themselves, typically file in person at the clerk's office located at the Ronald Reagan Federal Building in Harrisburg.

- Receive your case number and automatic stay notice. The court issues these immediately upon filing, and the automatic stay takes effect at that moment.

Failure to follow local district rules may cause immediate dismissal even when national forms are completed properly. The Middle District of Pennsylvania has specific local rules governing document formatting, filing deadlines, and required attachments that differ from other districts.

Pro Tip: If you face an imminent foreclosure sale or wage garnishment in the Harrisburg area, ask your attorney about filing a skeleton petition first. A skeleton petition triggers the automatic stay immediately with minimal paperwork, buying you time to complete the full filing within 14 days.

Types of bankruptcy petitions and their differences

Not all bankruptcy petitions are the same. The type you file depends on who initiates the case and which chapter of the Bankruptcy Code applies to your situation.

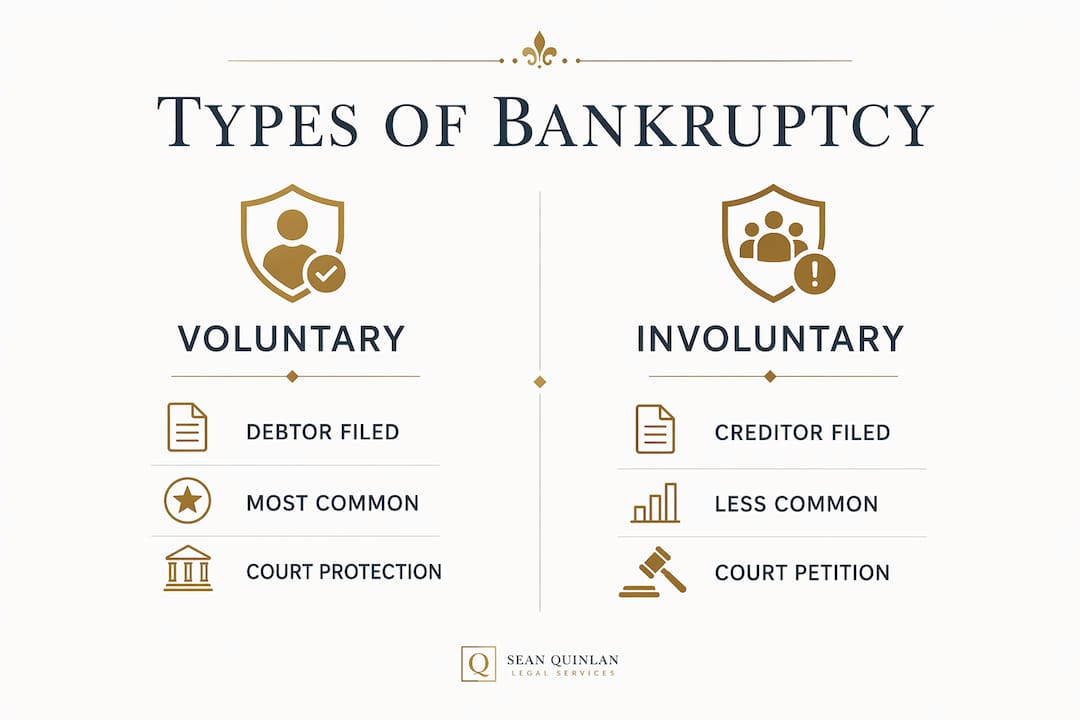

Voluntary vs. involuntary petitions

A voluntary petition is filed by the debtor, meaning you choose to seek bankruptcy protection. This is by far the most common type for individuals in Central Pennsylvania. An involuntary petition is filed by creditors against a debtor who owes them money. Involuntary petitions have strict requirements: generally, three or more creditors with combined unsecured claims of at least $18,600 must join the filing. Involuntary bankruptcy is rare for individuals and far more common in business contexts.

Chapter 7 vs. Chapter 13 petitions

The two most relevant chapters for individual filers are Chapter 7 and Chapter 13. Here is how they compare:

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Who qualifies | Must pass means test | Must have regular income |

| Duration | 3 to 4 months to discharge | 3 to 5 year repayment plan |

| Asset treatment | Non-exempt assets may be liquidated | Keep assets, repay debts over time |

| Best for | Unsecured debt relief (credit cards, medical bills) | Saving a home from foreclosure |

| Petition complexity | Moderate | High, due to repayment plan schedules |

| Pro se filing rate | 8 to 10% of cases | Rare and risky |

Chapter 13 petitions involve more detailed schedules and documentation because they require a court-approved repayment plan spanning three to five years. This added complexity is one reason why self-represented Chapter 13 filers face significantly higher dismissal rates than those with legal counsel.

For Pennsylvania residents weighing their options, a detailed comparison of Chapter 7 vs. Chapter 13 can help clarify which path fits your income, assets, and goals before you commit to a filing.

What happens after filing a bankruptcy petition?

Filing the petition is the beginning of the process, not the end. Once your case number is assigned and the automatic stay is in place, a structured sequence of events follows.

- Automatic stay takes effect immediately. Creditors must stop all collection activity, including phone calls, lawsuits, repossessions, and foreclosure proceedings. Violations of the automatic stay can expose creditors to sanctions.

- A bankruptcy trustee is assigned. The trustee reviews your petition and schedules for accuracy, looking for undisclosed assets, recent large transfers, or inconsistencies with your tax records. The trustee closely scrutinizes petition accuracy, and even small undisclosed assets can jeopardize the entire case outcome.

- The 341 meeting of creditors is scheduled. This meeting occurs 20 to 50 days after filing. You must appear in person or by phone, answer questions under oath about your finances, and confirm the accuracy of your petition. Creditors may attend but rarely do in straightforward cases.

- Discharge or repayment plan confirmation follows. In Chapter 7, if no objections arise and the trustee finds no hidden assets, discharge typically occurs within three to four months of filing. In Chapter 13, the court must confirm your repayment plan before you begin making payments to the trustee.

- Some debts survive discharge. Discharge is not guaranteed for all obligations. Most student loans, alimony, child support, recent tax debts, and debts arising from fraud are excluded from discharge regardless of chapter.

- Post-filing compliance is mandatory. You must complete a debtor education course before discharge, respond to trustee requests promptly, and make all required plan payments in a Chapter 13 case.

Key takeaways

A bankruptcy petition is the formal legal filing that starts your case, triggers the automatic stay, and requires complete and accurate financial disclosure to avoid dismissal or fraud penalties.

| Point | Details |

|---|---|

| Petition triggers automatic stay | Filing immediately halts creditor actions including garnishments, foreclosures, and collection calls. |

| Accuracy is legally required | Petition signatures are under penalty of perjury; omissions can result in fraud charges and case dismissal. |

| Chapter choice shapes the petition | Chapter 7 petitions are simpler; Chapter 13 requires a full repayment plan and more detailed schedules. |

| Local court rules matter | The Middle District of Pennsylvania has specific filing rules that differ from national defaults. |

| Discharge is not automatic | Certain debts like student loans and alimony survive bankruptcy regardless of which chapter you file. |

What I've learned from watching clients navigate this process

By Atry. Sean Quinlan

After working with clients across Harrisburg, Camp Hill, and surrounding counties, the pattern I see most often is not a lack of willingness to disclose. It is a genuine misunderstanding of what "complete" disclosure actually means. People forget about a security deposit they paid three years ago, or they fail to list a car that a family member is driving. The trustee finds it anyway. What looked like an oversight now looks like concealment.

The second most common mistake is treating the petition as a finish line rather than a starting point. Clients sometimes relax after filing, miss a trustee document request, or skip the debtor education course. Any of these can derail a case that was otherwise solid.

I also want to address the skeleton petition strategy directly. Filing a bare-bones petition to stop an imminent foreclosure or garnishment is a legitimate and sometimes necessary tactic. But the 14-day deadline to file complete schedules is firm. I have seen cases dismissed because the filer did not understand that the skeleton filing was a temporary measure, not a complete one. If you are considering this route in Cumberland County or Dauphin County, do not do it without guidance.

Finally, the Middle District of Pennsylvania enforces its local rules without much tolerance for pro se errors. The national forms are a floor, not a ceiling. Local formatting requirements, cover sheet rules, and electronic filing protocols add layers that catch unprepared filers off guard. Filing bankruptcy is a legal right. Filing it correctly requires preparation.

— Atry. Sean Quinlan

Get professional help with your bankruptcy petition in Pennsylvania

Facing financial pressure in Harrisburg, Camp Hill, or anywhere in Central Pennsylvania is stressful enough without navigating complex court procedures alone. Pennsylvania DUI Attorney, through the practice of Sean P. Quinlan, provides personalized guidance on bankruptcy petition preparation, chapter selection, and local court compliance for clients across Cumberland County, Dauphin County, and York County.

Whether you need to stop a foreclosure quickly or build a structured path out of debt, Sean P. Quinlan brings direct experience with the Middle District of Pennsylvania's requirements to every case. Reach out today to schedule a consultation and get a clear picture of your options. Visit the bankruptcy services page to learn how personalized legal support can protect your financial future from the moment you file.

FAQ

What is a bankruptcy petition in simple terms?

A bankruptcy petition is the official legal document you file with a federal court to start a bankruptcy case. Filing it immediately triggers the automatic stay, which stops most creditor collection actions.

How much does it cost to file a bankruptcy petition in 2026?

Filing fees in 2026 are $338 for Chapter 7 and $313 for Chapter 13. Low-income filers may qualify for a fee waiver or installment payment plan by submitting the appropriate official forms.

What is required before you can file a bankruptcy petition?

You must complete a mandatory credit counseling course from an approved provider within 180 days before filing. The course takes 60 to 90 minutes and costs between $15 and $50, and the certificate must be submitted with your petition.

What happens at the 341 meeting after filing?

The 341 meeting of creditors is scheduled 20 to 50 days after you file your petition. You must appear and answer questions under oath about your financial disclosures, and the trustee uses this meeting to verify the accuracy of your petition.

Can all debts be discharged through a bankruptcy petition?

No. Debts such as most student loans, alimony, child support, and recent tax obligations typically survive bankruptcy and are not discharged regardless of which chapter you file under.