A bankruptcy stay, formally known as the automatic stay, is a federal legal injunction that halts virtually all creditor collection activities the instant a bankruptcy petition is filed. No court hearing is required and no judge needs to sign an order. The protection is immediate and applies to wage garnishments, lawsuits, foreclosures, repossessions, and collection calls. For individuals in Camp Hill, Harrisburg, Cumberland County, Dauphin County, and York County facing mounting debt pressure, understanding the automatic stay is the first step toward regaining control of your financial situation.

What is bankruptcy stay and what does it actually stop?

The automatic stay is defined under 11 U.S.C. § 362 and takes effect the moment a bankruptcy petition is filed, requiring no court order. It functions as a federal injunction, which means it carries the full weight of federal law and is enforceable against virtually every creditor simultaneously. That distinction matters because a traditional injunction requires a court hearing, a bond, and a judge's signature. The automatic stay requires none of those things.

The scope of the stay is broad. Here is what it stops immediately upon filing:

- Wage garnishments currently deducting money from your paycheck

- Foreclosure proceedings on your home, including scheduled sheriff sales in Cumberland or Dauphin County

- Vehicle repossessions by lenders or finance companies

- Lawsuits filed by creditors seeking money judgments

- Collection calls, letters, and harassment from debt collectors

- Bank levies and freezes on deposit accounts

- Utility shutoffs for a limited period after filing

The stay gives you what attorneys call "breathing room." It does not erase your debts, but it stops the bleeding while you work through the bankruptcy process. For someone in Harrisburg facing a foreclosure sale next week, filing a Chapter 7 or Chapter 13 petition before that sale date can halt the entire proceeding.

Pro Tip: Document every creditor contact you receive after filing. Courts can award actual damages and attorney fees for willful stay violations, so a paper trail is your strongest enforcement tool.

How long does the bankruptcy stay last under Chapter 7 and Chapter 13?

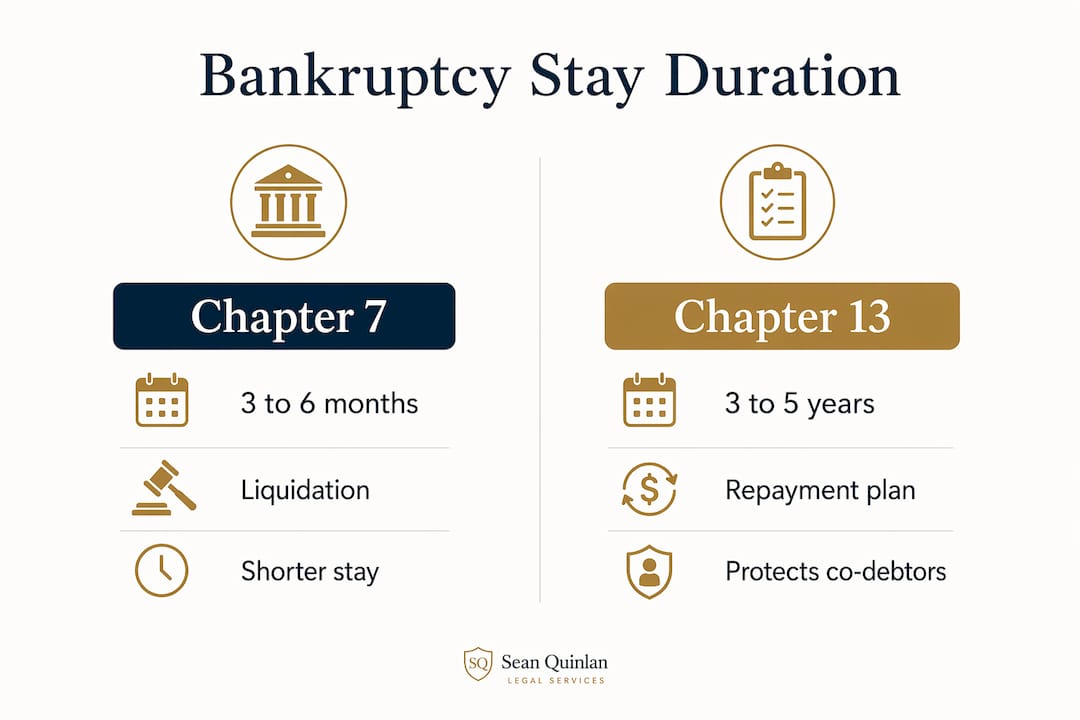

The duration of the automatic stay depends entirely on which chapter of bankruptcy you file. The two most common options for individuals are Chapter 7 and Chapter 13, and they produce very different timelines.

Chapter 7 stay duration typically runs three to six months, which is the time it takes to complete the liquidation process and receive a discharge. Once the court issues the discharge order or closes the case, the stay ends. For most unsecured debts like credit cards and medical bills, the discharge itself eliminates the obligation, so the stay's expiration is largely irrelevant at that point. The creditor no longer has a valid claim to collect.

Chapter 13 offers a longer and more layered form of protection. The stay remains in place through the confirmation of your repayment plan and then continues for the entire three to five year repayment period. That extended protection is particularly valuable if you are trying to save a home from foreclosure in York County or catch up on car payments while keeping the vehicle.

| Feature | Chapter 7 | Chapter 13 |

|---|---|---|

| Stay duration | 3 to 6 months | 3 to 5 years (full repayment plan) |

| Co-debtor protection | Not included | Included for consumer debts |

| Foreclosure relief | Temporary halt only | Can cure arrears over plan term |

| Stay ends when | Discharge or case closure | Plan completion or case dismissal |

| Best for | Unsecured debt elimination | Saving secured assets like a home |

One critical distinction: Chapter 13 protects co-debtors such as family members or friends who co-signed a loan, while Chapter 7 does not. If your spouse co-signed a personal loan and you file Chapter 7, the lender can still pursue your spouse. Chapter 13's co-debtor stay prevents that collection action during the repayment period.

Pro Tip: Serial filers face shortened or limited stay protections under federal law. If you have filed bankruptcy within the past year and had a case dismissed, the stay may only last 30 days or may not apply at all unless you obtain a court extension before filing.

What are the exceptions and how can creditors challenge the stay?

The automatic stay is powerful, but it is not absolute. Specific statutory exceptions under 11 U.S.C. § 362(b) allow certain proceedings to continue regardless of a bankruptcy filing. Knowing these limits protects you from false assumptions about your coverage.

The most common exceptions include:

- Criminal proceedings. A bankruptcy filing does not stop a criminal prosecution or sentencing. If you face criminal charges in Cumberland County alongside your financial problems, those proceedings move forward independently.

- Certain tax actions. The IRS and Pennsylvania Department of Revenue can still conduct tax audits, issue tax deficiency notices, and demand tax returns. They cannot collect, but they can assess.

- Child support and alimony. Domestic support obligations are entirely exempt from the stay. A family court in Dauphin County can still enforce a support order against you after you file.

- Evictions where the lease ended before filing. If your landlord obtained a judgment for possession before you filed bankruptcy, the stay may not prevent the eviction from proceeding.

- Certain pension loan repayments. Loans from qualified retirement plans like a 401(k) are generally excluded from stay protection.

Beyond these statutory exceptions, creditors can actively seek to end the stay by filing a motion for relief from stay with the bankruptcy court. A creditor must show either that the debtor lacks equity in the property or that the property is not adequately protected. For example, if you stopped making mortgage payments and the home has no equity, the lender has strong grounds to request relief. Courts must rule within 30 days on certain relief motions, or the stay terminates automatically for that specific property. That deadline creates urgency for both sides.

If a creditor violates the stay without court permission, you have legal recourse. Courts award actual damages including attorney fees for willful violations. Contact your bankruptcy attorney immediately if a creditor continues collection activity after your filing date.

What is the practical impact of the stay for Central Pennsylvania residents?

The real-world effect of the automatic stay depends on where you are in the debt cycle when you file. For someone in Camp Hill whose wages are already being garnished, the stay stops that garnishment with the next paycheck cycle after filing. For a homeowner in York County with a sheriff sale scheduled, filing before that date cancels the sale and forces the lender back to the negotiating table.

| Situation | Effect of automatic stay | What happens after stay ends |

|---|---|---|

| Wage garnishment | Stops immediately upon filing | Resumes if debt survives bankruptcy |

| Home foreclosure | Halts sale and proceedings | Lender may refile if arrears not resolved |

| Vehicle repossession | Prevents repossession during case | Lender can repossess if payments not resumed |

| Credit card lawsuits | Freezes all pending litigation | Discharged in Chapter 7; managed in Chapter 13 |

| Utility shutoff | Delays shutoff for 20 days | Service may be discontinued after period ends |

One area where people frequently misunderstand the stay involves credit reporting. The automatic stay stops creditor collection actions, but it does not erase the bankruptcy from your credit report. Chapter 7 remains on your credit report for 10 years, while Chapter 13 stays for 7 years. The credit impact is real and long-term, but it fades over time as you rebuild. The stay's value is immediate protection, not credit repair.

For individuals in Harrisburg or Cumberland County who are weighing their options, the stay also creates space to negotiate. During the period when creditors cannot act, you and your attorney can evaluate whether a Chapter 13 repayment plan is feasible, whether certain assets can be protected under Pennsylvania exemptions, and whether a structured resolution serves you better than liquidation. Understanding your bankruptcy options before filing helps you use the stay strategically rather than reactively.

Strategic filing timing is one of the most underutilized tools in bankruptcy practice. Attorneys advise clients to file before critical deadlines such as a foreclosure sale date or a bank levy to maximize the stay's protective effect. Waiting even one day too long can mean losing an asset that the stay would have preserved.

Key takeaways

The automatic stay is the single most powerful immediate protection bankruptcy law provides, and filing at the right moment determines how much of that protection you actually receive.

| Point | Details |

|---|---|

| Instant federal protection | The automatic stay activates the moment you file, with no court order required. |

| Chapter duration difference | Chapter 7 stay lasts 3 to 6 months; Chapter 13 stay covers the full 3 to 5 year repayment plan. |

| Co-debtor coverage | Only Chapter 13 extends stay protection to co-signers on consumer debts. |

| Exceptions exist | Criminal cases, domestic support, and certain tax actions continue despite the stay. |

| Violations carry penalties | Creditors who willfully violate the stay face actual damages and attorney fee awards. |

What I have seen attorneys get wrong about the automatic stay

By Atty. Sean Quinlan

After working with clients across Cumberland, Dauphin, and York counties, the single most damaging misconception I encounter is the belief that the automatic stay lasts until all debts are paid. It does not. The stay is a temporary shield, not a permanent resolution. Clients who misunderstand this sometimes delay taking the next steps in their case, only to find that a creditor has obtained relief from stay and resumed collection while they were waiting.

The second issue I see regularly is clients who fail to document creditor violations. When a debt collector calls after a filing date, that call is potentially a sanctionable act. Courts take willful violations seriously, and the enforcement mechanisms exist precisely to give debtors teeth. But you need a record. Save voicemails, screenshot texts, and log every contact with a date and time.

Filing timing is where experienced counsel makes the biggest difference. I have seen clients in Harrisburg lose homes to sheriff sales because they waited three days too long to file. The Chapter 7 vs. Chapter 13 decision also directly affects how long the stay protects you and whether your co-signers are covered. These are not abstract legal distinctions. They determine real outcomes for real families. If you are facing creditor pressure in Central Pennsylvania, the time to act is before the deadline, not after.

— Atty. Sean Quinlan

Protect your rights with experienced Pennsylvania bankruptcy counsel

The automatic stay is one of the most powerful tools in bankruptcy law, but creditors can and do challenge it. Navigating a motion for relief from stay, documenting violations, and timing your filing correctly requires legal knowledge that goes beyond general research.

Pennsylvania DUI Attorney, led by Attorney Sean P. Quinlan, provides experienced legal guidance for individuals facing creditor actions, foreclosure, wage garnishment, and debt collection in Camp Hill, Harrisburg, Cumberland County, Dauphin County, and York County. If you are considering bankruptcy and want to understand how the automatic stay can protect you, contact our office for a consultation. Visit our legal services page to get started and take the first step toward protecting your financial future.

FAQ

What is an automatic stay in bankruptcy?

An automatic stay is a federal court injunction that halts all creditor collection activities the moment a bankruptcy petition is filed, including lawsuits, wage garnishments, foreclosures, and repossessions, without requiring a separate court order.

How long does a bankruptcy stay last?

The duration depends on the chapter filed. Chapter 7 stays last approximately three to six months until discharge, while Chapter 13 stays remain in effect for the entire three to five year repayment plan period.

Can a creditor get around the bankruptcy stay?

Yes. Creditors can file a motion for relief from stay and must show the debtor lacks equity in the property or that the property is not adequately protected. Courts must rule within 30 days on certain motions or the stay terminates automatically for that property.

Does the bankruptcy stay stop criminal cases?

No. Criminal proceedings are among the statutory exceptions under 11 U.S.C. § 362(b) and continue regardless of a bankruptcy filing. The stay applies only to civil collection actions, not criminal prosecution.

What happens if a creditor violates the automatic stay?

A creditor who willfully violates the stay faces court sanctions including actual damages and attorney fees. You should document every contact and notify your bankruptcy attorney immediately so enforcement action can be taken.