After an auto or truck accident in Pennsylvania, receiving a settlement feels like relief. But for many injured people, that relief quickly turns to confusion when medical bills, insurance demands, and repayment claims start arriving. You may have assumed the settlement would simply pay your bills and put money in your pocket. The reality is significantly more complicated, and understanding how medical expenses are handled before, during, and after settlement can mean the difference between walking away financially whole or still owing thousands of dollars to hospitals and insurers.

Table of Contents

- The journey of your medical bills after an accident

- Who pays medical bills in Pennsylvania injury settlements?

- Medical liens and subrogation: What you must know

- How to maximize your net settlement after medical bills

- A hard truth: Why your final payout is almost never what you expect

- Get help with your Pennsylvania accident claim

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple payors involved | Your medical bills may be paid by auto insurance, health plans, or government programs after an accident in Pennsylvania. |

| Liens and subrogation matter | Hospitals and insurers can often claim part of your settlement to recover their costs, so your take-home amount can be reduced. |

| Order of payment affects you | The type of insurance you have and who pays first plays a major role in how much money you actually receive. |

| Experience helps negotiation | An experienced Pennsylvania attorney can often reduce what you owe and help you keep more of your settlement. |

The journey of your medical bills after an accident

To understand why your bills aren't always simply "covered," let's walk through the journey your medical expenses take after an accident.

When an auto or truck accident happens in Pennsylvania, your medical bills don't wait for a settlement to arrive. Treatment starts immediately, and so does the billing. The path those bills travel is rarely straightforward, and it typically involves multiple payors before any settlement check is issued.

Here is how that journey usually unfolds:

-

Auto insurance pays first. Pennsylvania requires drivers to carry Personal Injury Protection (PIP), also known as first-party medical benefits. This coverage pays your medical bills directly, up to your policy limit, regardless of who caused the accident. Standard limits start at $5,000, but higher limits are available and worth carrying.

-

Health insurance steps in when auto coverage runs out. Once your PIP or MedPay (Medical Payments coverage) is exhausted, your health insurer typically becomes responsible for remaining medical expenses. Your health plan will apply its own deductibles, copays, and network restrictions, just as it would for any other medical event.

-

Out-of-pocket costs accumulate. If you have gaps in coverage or your treatment exceeds what either insurance will cover, you may be paying expenses directly. Specialists, follow-up care, and certain therapies often fall into this category.

-

Providers assert medical liens. A medical lien is a legal claim that a hospital, doctor, or insurer files to secure repayment from your future settlement. If a provider treated you and has not been fully paid, they can place a lien on your settlement proceeds. This gives them a legal right to payment before you receive your share.

-

Settlement funds are distributed to lienholders first. When your case settles, your attorney receives the gross settlement. Outstanding liens and unpaid bills must typically be satisfied from those funds before you receive your net payment.

-

You receive your net share. After attorney fees, litigation costs, and lienholder payments, the remaining balance comes to you.

As noted in the Pennsylvania Medical Lien Calculator, the process for handling medical bills in auto accidents can involve both health and payor sources and later subrogation during settlement, making it essential to track all bill sources from day one.

For a more detailed breakdown of each stage, see this guide on auto injury compensation steps in Pennsylvania, which walks through timelines and legal considerations at each phase.

Pro Tip: Missing deadlines for notifying your auto insurer or health plan about your accident can result in denied claims or reduced reimbursements. Notify all relevant insurers in writing within days of the accident, not weeks.

It also helps to familiarize yourself with key Pennsylvania personal injury terms so you can follow conversations with your attorney and insurance adjusters without confusion.

Who pays medical bills in Pennsylvania injury settlements?

Now that you've mapped your medical bills' journey, it's important to see exactly who foots the bill at each stage and how it may affect your total recovery.

Pennsylvania operates under a specific payment priority system for auto accident medical bills. Understanding this order can help you anticipate how your settlement funds will be allocated and what repayment demands you might face.

Common sources of medical payment after an accident:

- Auto insurance (PIP/MedPay): Pays first, up to policy limits, without regard to fault.

- Health insurance (private plans): Covers bills once PIP is exhausted; has subrogation rights (the right to seek repayment from your settlement).

- Medicare and Medicaid: Federal programs with very strong reimbursement rights under federal law.

- ERISA-governed employer health plans: Subject to federal rules that can preempt (override) Pennsylvania state law protections, making lien reductions harder to negotiate.

- Out-of-pocket payment: Covers gaps when no other source applies.

| Primary payor | When it applies | Has subrogation/lien rights? | Negotiable? |

|---|---|---|---|

| Auto insurance (PIP) | First, up to policy limits | Generally no | No |

| Private health insurance | After PIP is exhausted | Yes, under state law | Often yes |

| Medicare | Whenever it pays | Yes, under federal law | Limited |

| Medicaid | Whenever it pays | Yes, under federal law | Very limited |

| ERISA employer plan | After PIP, based on plan terms | Yes, federal preemption applies | Difficult |

One critical point that surprises many injured Pennsylvanians is the role of ERISA plans. The Employee Retirement Income Security Act governs most employer-sponsored health plans, and it can give those plans powerful rights to recoup every dollar they paid on your behalf, even if your total settlement doesn't fully compensate your injuries. As noted in the Pennsylvania Medical Lien Calculator, responsibility for payment can differ, and ERISA health plans may make subrogation harder to reduce, which is a factor your attorney must address early in your case.

For a broader understanding of your rights after a crash, review this resource on auto accident rights in Pennsylvania before engaging with any insurer.

Pro Tip: Ask your attorney to identify all payors and their legal authority before settling. Knowing whether your health plan is governed by ERISA or Pennsylvania state law makes a significant difference in how much you can negotiate down your repayment obligations.

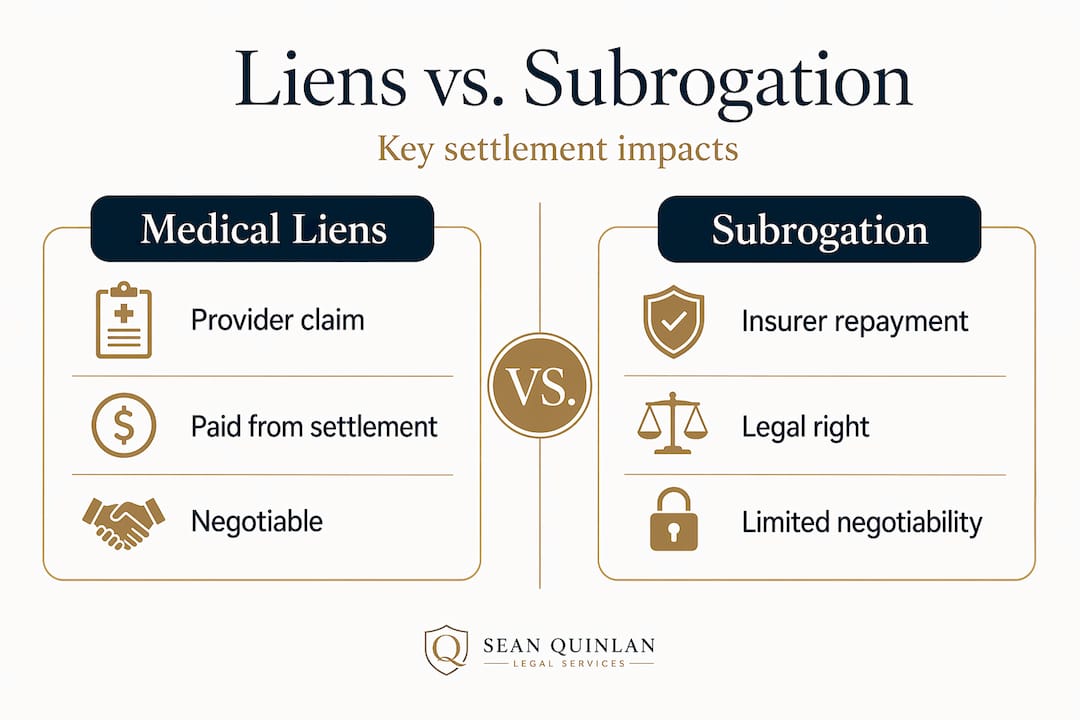

Medical liens and subrogation: What you must know

Understanding who pays is only part of the equation; figuring out what you actually owe because of liens or insurer "payback" is critical.

Two terms come up repeatedly in Pennsylvania injury settlements: medical liens and subrogation. Both involve parties seeking repayment from your settlement proceeds, but they work differently and carry different legal weight.

A medical lien is a legal claim filed by a healthcare provider, hospital, or insurer asserting a right to be paid from your settlement. Liens are recorded documents that attach to your settlement funds, meaning your attorney cannot simply distribute the money without addressing them.

Subrogation is the process by which an insurer who paid your medical bills "steps into your shoes" and seeks reimbursement from the party responsible for your injuries or from your settlement. Your health plan paid the bills; now they want that money back once you've recovered it from the at-fault party.

Common types of medical liens in Pennsylvania injury cases:

- Hospital and provider liens: Filed directly by hospitals or treatment centers for unpaid balances.

- Health insurance subrogation claims: Your private health insurer asserting its right to repayment.

- Medicare conditional payment demands: The federal government issues these formally, and they carry strict legal deadlines.

- Medicaid estate recovery claims: Pennsylvania's Medicaid program (Medical Assistance) may seek repayment.

- Workers' compensation liens: Relevant when workplace accidents intersect with auto injuries.

- ERISA plan reimbursement demands: Among the hardest to reduce due to federal preemption.

According to the Pennsylvania Medical Lien Calculator, liens can allow providers and plans to be reimbursed from your settlement proceeds, and when ERISA rules apply, they may significantly complicate any effort to negotiate a reduced payoff.

Pennsylvania law does offer some protections for injured claimants. The state's "made whole" doctrine, for example, argues that an insurer should not recover subrogation until the injured party has been fully compensated for all losses. However, ERISA plans routinely argue that federal law overrides this state protection, and courts have frequently sided with the plans.

This complexity is exactly why your attorney must identify the nature of each lien and the governing law before any settlement discussion begins. Understanding your personal injury rights in PA is essential before agreeing to any settlement terms.

To learn more about the broader process of seeking compensation after an injury, this resource on how to pursue compensation provides clear guidance on timelines and legal strategy.

One important statistic to keep in mind: studies of personal injury settlements suggest that lien payoffs can consume anywhere from 20% to 40% of gross settlement funds in cases involving significant medical treatment. That figure rises substantially when Medicare, Medicaid, or ERISA plans are involved.

How to maximize your net settlement after medical bills

With liens and subrogation in mind, here's how you can improve your actual settlement after all medical bills are addressed.

Taking a proactive approach to medical bill management throughout your case gives you the best chance of keeping more of your settlement. These steps are practical and actionable, regardless of how complex your case becomes.

-

Notify all relevant insurers immediately. Contact your auto insurer, health insurer, and any government programs the moment you receive treatment. Late notification can result in denied coverage or reduced benefits.

-

Request itemized bills from every provider. Itemized billing shows each service charged. Errors are common in hospital billing, and you cannot identify mistakes without a line-by-line breakdown.

-

Track all out-of-pocket expenses. Keep receipts for co-pays, prescriptions, transportation to appointments, and any medical equipment. These expenses may increase your overall claim value.

-

Work with an attorney before settling. An experienced Pennsylvania personal injury attorney can identify all outstanding liens, estimate net recovery before you agree to any figure, and negotiate repayment amounts down.

-

Negotiate medical liens directly. Many providers, particularly hospitals and health insurers (excluding Medicare and Medicaid), will accept a reduced lien amount to settle the debt. This is especially true when the total settlement is limited and would not fully compensate your injuries.

-

Resolve Medicare and Medicaid claims carefully. Federal programs have strict reporting and repayment requirements. Failing to satisfy Medicare's conditional payment demand can result in penalties and double damages.

| Lien/bill type | Typical portion of gross settlement consumed | Negotiability |

|---|---|---|

| Private health insurance subrogation | 10% to 25% | Moderate to high |

| Hospital/provider liens | 5% to 20% | Often negotiable |

| Medicare conditional payments | 10% to 30% | Limited, formal process required |

| Medicaid claims | 5% to 15% | Very limited |

| ERISA plan demands | 15% to 35% | Difficult; federal rules apply |

Pro Tip: Never accept a settlement offer without first obtaining written payoff amounts from every lienholder. Settling without this information can leave you legally obligated to pay liens that exceed what you thought you would owe, effectively leaving you in debt after your case "resolves."

For more guidance on protecting yourself legally after an accident, review these legal tips after a car accident in Pennsylvania, which cover documentation, timing, and common mistakes to avoid.

Subrogation rights may be limited by the type of plan, but proper documentation and negotiation are what separate clients who walk away with meaningful compensation from those who don't.

A hard truth: Why your final payout is almost never what you expect

There is something important that even well-prepared injury victims often discover only after settlement papers are signed: the number on the settlement agreement and the number that actually reaches your bank account are very different figures. This gap is not the result of dishonesty or error. It is the predictable outcome of a system in which multiple parties have legal claims to your recovery.

Many clients arrive at settlement expecting to receive the headline figure, minus only attorney fees. What they encounter instead is a waterfall of deductions: attorney fees, case costs, auto insurer repayments, health plan subrogation demands, Medicare or Medicaid repayments, and provider liens. In complex truck accident cases or cases involving long-term treatment, these deductions can easily consume half of the gross settlement.

Common myths versus actual client experiences:

- Myth: "The settlement pays all my bills automatically." Reality: Bills must be individually tracked, and some require formal payoff agreements before funds are released.

- Myth: "My health insurer already got paid, so they're done." Reality: If your health insurer paid accident bills, they typically have subrogation rights and will assert a claim against your settlement.

- Myth: "I can negotiate any lien down to pennies on the dollar." Reality: Medicare, Medicaid, and ERISA plans have limited negotiability, and federal law controls the outcome.

- Myth: "A larger settlement means I'll keep more." Reality: Higher settlements can trigger larger proportional lien demands, particularly from Medicare and ERISA plans.

"Settlement shock" is a term used informally among injury attorneys to describe the moment a client learns their net recovery is far lower than the gross settlement figure suggests. Even clients who were warned often find the final accounting hard to accept.

Understanding the importance of injury lawsuits and what an experienced attorney actually does on your behalf helps set realistic expectations. An attorney's job is not just to win a settlement but to manage the aftermath, including negotiating liens down, challenging improper subrogation claims, and ensuring federal reporting obligations are met. Learn more about the role of an injury attorney throughout this process to understand what effective representation looks like.

Get help with your Pennsylvania accident claim

Navigating medical bills, liens, subrogation demands, and insurer negotiations after an auto or truck accident is genuinely difficult. If you find these rules and negotiations overwhelming, remember that help is available.

Working with an experienced Pennsylvania personal injury attorney protects your interests at every stage of your case. From identifying all lienholders to negotiating payoffs and ensuring you don't settle for less than your case is worth, skilled legal representation can mean thousands of extra dollars in your pocket when it matters most.

At pennsylvaniadui.attorney, Sean Quinlan and his team have extensive experience handling auto accident and personal injury claims throughout Pennsylvania. Whether you need help understanding your options or want someone to manage your entire case, you can get the support you deserve. Visit the auto accidents page or explore personal injury legal support to schedule a free case review and take the first step toward a fair recovery.

Frequently asked questions

Who pays my medical bills after an auto accident in Pennsylvania?

Typically, your auto insurance (PIP or MedPay) pays first up to policy limits, then health insurance covers the remainder, and unpaid balances may ultimately be resolved through your settlement proceeds.

Can my health insurance take money from my injury settlement?

Yes. If your health insurer paid accident-related bills, they commonly assert subrogation rights and can seek repayment from your settlement, with different rules applying to ERISA plans versus state-regulated plans.

What if I can't pay my medical bills before my settlement arrives?

Hospitals and providers can agree to defer payment until your settlement is finalized or may formally assert a lien that secures their right to be paid from settlement proceeds.

Do all settlements have to pay back Medicare or Medicaid?

Yes, federal law generally requires repayment to Medicare and Medicaid when those programs covered accident-related treatment, and these reimbursement rights are among the strongest of any payor.

Can a lawyer help reduce what I owe from my settlement?

Yes, skilled attorneys regularly negotiate reduced payoffs with private insurers and providers, and they can also navigate the formal processes required to minimize Medicare and Medicaid repayment demands.